Interest charge on ITC Value: Federation of Automobile Dealers Associations writes to GST Council - What they said and demanded?

In a major development for auto industry, the Federation of Automobile Dealers Associations (FADA) has sent a representation to the GST Council on charge of interest on Gross Value instead of Net of Input Tax Credit (ITC) value, while making the GST payment on monthly basis.

In a major development for auto industry, the Federation of Automobile Dealers Associations (FADA) has sent a representation to the GST Council on charge of interest on Gross Value instead of Net of Input Tax Credit (ITC) value, while making the GST payment on monthly basis. FADA President, Ashish Harsharaj Kale has commented on the issue. Here is the FULL TEXT of his statement:-

“Many of our members are Small Family run businesses located in Tier 2&3 towns and face difficulties in GST Compliances or returns, many a times due to system mismatches not in their Control. However, because of the nature of The Auto Retail Trade, the Business Turnover and Input Tax Credit Available is quite High.

"In the Case of a Delayed Return, the ITC in balance as on the due date for filing the return has no relevance with regard to the interest liability u/s 50 of the Act, which provides for levy interest on late payment of GST on tax liability (which has to be Net Tax Liability as ITC is already in electronic credit ledger in control of GSTN). The issue in hand is that in the event of any delay in payment of tax liability, whether the interest payable u/s 50 shall be on the net amount payable by the assessee (net of ITC) or on the gross amount before ITC is set off. This has resulted in undue hardship to automobile dealers (members of F A D A) across the country.

"It is the Revenue Department’s interpretation that since Input tax credit balance in the ‘Electronic Credit Ledger’ cannot be treated as the tax paid, unless it is debited in the said credit ledger while filing the return for off-setting the amount in the ‘Liability Ledger’, the interest liability u/s 50 of the Act is mandatorily attracted on the entire tax remained unpaid beyond the due date prescribed. The ITC in balance as on the due date for filing the return has no relevance with regard to the interest liability under section 50 of the Act. It is immaterial whether the self-assessed tax is paid through ITC or the Cash. Once the payment is beyond the prescribed date, interest liability is attracted on the entire tax amount.

“The proposal to charge interest on net of ITC value instead of Gross had been already recommended by the GST Council in its 31st meeting held on 22.12.2018. However, the same could not be passed due to Parliament dissolution for four months.

F A D A has, therefore, requested that the same gets approved in the upcoming GST Council meet on 21st June’19 and that the interest provided should be calculated on net tax liability instead of gross tax liability. We hope that the Request is Considered by H’ble GST Council which will further help Auto Dealers in Ease of Doing Business by implementing its decision taken in 31st GST Council Meet.

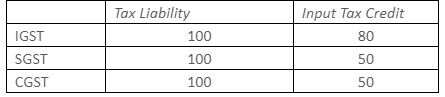

Let us suppose the following figures for filing the GSTR-3B:

Suppose, GSTR-3B had not been filed by 20th of the following month, then interest is to be calculated on entire Rs. 100 (IGST), Rs. 100(SGST) and Rs. 100(CGST) instead on Rs. 20, 50 and 50 respectively from the due date of filing of GSTR-3B till the actual date of filing.

"F A D A has also suggested to make necessary amendments in the law that interest amount should not be charged on retrospective basis and on gross amount but should only be charged on balance (net) amount payable and to suitably amend Section 41(2) by inserting a proviso to the effect that any delay in filing the return shall not lead to payment of interest u/s 50 to the extent of amount already lying to the credit of electronic credit ledger," as per a statement released.

It has also demanded to issue a suitable order to remove administrative difficulty on implementation of section 50 to capture the spirit of law and to issue necessary administrative directions to field formations not to take any coercive action in view of the GST Council decisions.

05:19 PM IST

Budget 2020 Reaction: What Federation Of Automobile Dealers Associations has to say

Budget 2020 Reaction: What Federation Of Automobile Dealers Associations has to say FADA releases Nov 2019 Vehicle Registration Data; extended cheer to dealer community- Check key details

FADA releases Nov 2019 Vehicle Registration Data; extended cheer to dealer community- Check key details FADA writes to SIAM to upgrade to Market Share Calculation by way of Vahan Registrations - FULL TEXT of letter

FADA writes to SIAM to upgrade to Market Share Calculation by way of Vahan Registrations - FULL TEXT of letter Passenger vehicle retail sales dip 1 percent in May: FADA

Passenger vehicle retail sales dip 1 percent in May: FADA Dealership body appeals to govt to keep GST rate at 0.5-1% on used cars

Dealership body appeals to govt to keep GST rate at 0.5-1% on used cars