Can PSU bank merger help them outshine private banks' deposit growth?

Moody's believes that PSU bank merger will be credit positive but banks still need a lot of money for recapitalisation.

Key Highlights:

- Cabinet approves merger plan for 21 PSBs

- Banks have gross NPAs up to Rs 8,29,335 crore in Q1FY18

- Moody's feel merger of PSBs is credit positive

Referring to Union Cabinet's decision on merger of public sector banks last week as 'credit positive', Moody's Investor Services on Monday said that the move will support the state-owned banks in exceeding private banks in deposit growth.

On August 23, 2017, Union cabinet chaired by Prime Minister Narendra Modi gave in-principle approval for public sector banks (PSBs) to merger with each other through an alternative mechanism (AM).

Moody's said, “This is credit positive because mergers would provide scale efficiency and improve the quality of corporate governance.”

Consolidation of PSBs comes at the backdrop of rising non-performing assets or bad loans. Bad loans in PSBs have resulted in higher provisions, deterioration in asset quality, higher slippages and thus lower earnings for banks -- not to forget their future lending is at stake.

As on June 2017, banks listed on stock exchanges saw sharp rise of 34.17% in NPAs to Rs 8,29,335 crore compared to Rs 6,18,109 crore in the corresponding period of the previous year.

According to Moody's, poor corporate governance has been structural credit weakness at public-sector banks, and managing all 21 has proven to be unwieldy for the government, which has been unable to pay sufficient attention to key issues such as long-term strategies and human resources.

“Consolidation would address some of these issues,” said Moody's.

One key thing that the consolidation would support PSBs would be in creating competitive advantage in regards to deposit growth.

“Consolidating public-sector banks also would help from a scale perspective. Public-sector banks are the dominant segment of India’s banking system, holding around 74% of all deposits,” says Moody's.

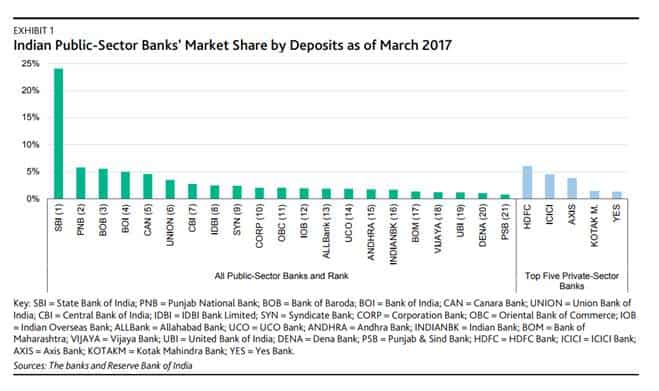

Sadly, except SBI none of other PSBs is large enough to have a competitive advantage compared to private banks.

A list of 16 PSBs still have lower than 5% deposit growth as on March 2017. SBI dominates with over 20% growth and while Punjab National Bank (PNB), Bank of Baroda (BoB) and Bank of India (BOI) hovering near 5%.

Deposits grew by 15.8% for the year ending March 31st 2017 as against 9.3% last year. Also the one-year bank deposit rate had moved from the range of 7-7.5% in FY16 to 6.5-7% by March 2017.

However, the consolidation decision is not something new to India, the move was first suggested in the year 1991 but came in headline after largest lender State Bank of India (SBI) decided to merger with six associates on May 2016.

The merger of SBI and associates has completed and after that there 21 more PSBs in picture.

Moreover, Moody's still feel that this move will not improve PSBs weak capitalisation. It said, “Notwithstanding the positive effect on corporate governance and scale efficiencies, any proposed mergers would not improve public-sector banks’ weak capitalisation.

After in-principle approval, the Banks will take steps in accordance with law and SEBI’s requirements. The final scheme will be notified by Central Government in consultation with the Reserve Bank of India.

ALSO READ:

10:44 AM IST

PSBs in PCA framework may not get govt's recap support

PSBs in PCA framework may not get govt's recap support