Future of Reliance Communication looks bleak, will exit from S&P BSE 200 index

RCom continues to face pressure from investors and analysts due to it’s heavy losses, net debt and rating downgrades. The company's total debt stood at Rs 45,000 crore by end of Q2FY18.

Key Highlights:

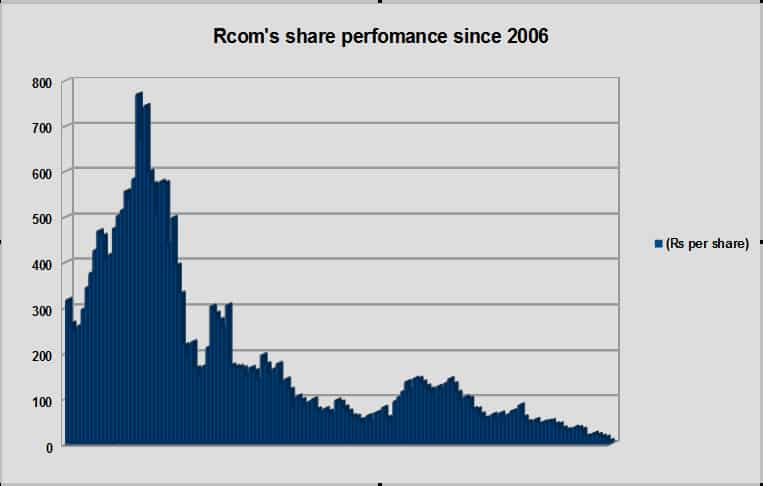

- RCom joined Sensex in the year 2006

- RCom shares continue to trade negative

- RCom's total debt at Rs 45,000 crore as on September 2017

Problems for Anil Ambani's Reliance Communication (RCOM) continues further as the company may be exiting from broader S&P BSE 200 index from next month.

Asia index - the S&P company which maintains major BSE stocks, has reconstituted the indices and the changes will be effective next month 18 December 2017.

Following such announcement, the Rcom's share price tumbled nearly 5% at the day's low of Rs 11.50 per piece on Monday after closing at Rs 12.05 per piece on BSE.

Last week on November 16, 2017, the company's share price faced heavy selling pressure – which led it to an all-time low of Rs 9.65 per piece. With this on year-on-year basis, Rcom's stocks have declined by over 76%.

However, this would be second exclusion from stock exchanges as earlier in August 2011, two shares namely Rcom and Reliance Infrastructure of Anil Dhirubhai Ambani Group, were removed from Sensex.

Rcom entered into the elite category of Sensex in 2006 just few months after being listed, and since then it has managed to even touch over Rs 800-mark. However, from January 2016, the RCOM stock which was near Rs 100-level, became more than half in February 2016 and closed near Rs 30 per share by end of December 2016.

Investors and analysts have been losing faith in Reliance Communication since start of FY18 mainly due to its continuous financial losses, lower capacity to repay debt and credit downgrades from various agencies.

Future of Rcom has become so bleak that on November 18, Moody's Investors Service withdrew corporate family rating of Rcom, citing a missed scheduled payment related to the company's dollar bond.

Not only this, HSBC a global research agency has decided to terminate equity research coverage of Rcom. Analysts at HSBC said, “ We believe that in its current form RCOM is likely to see a sharp decline in market share and we are sceptical about the company gaining much from a pure 4G approach. Our lower value for the core business is driven by the cut in EBITDA estimates as we factor in the shutdown of the 2G/3G business.”

On June 07, 2017, Ambani presented its debt payment plan to its lenders who approved it given the company time till December 2017 to pay the loans due. Rcom hoped to recover 60% of its total debt from two mergers namely with Aircel and Brookfield Infrastructure.

Ambani assured that both the deals will be completed by September 30, 2017 and the Rs 25,000 crore proceeds will be used to pay lenders. However, last month, both Aircel and Brookfield withdrew the schemes of arrangement in regards to demerger of wireless division of Rcom.

Now situation is such that Rcom has decided to shut down voice call service from December 01, and its customers can move to other networks by the end of the year.

While debt continues to increase from Rs 44,000 crore in Q1FY18 to Rs 45,000 crore by end of September 2017. Of this, Rs 25,000 crore is domestic debt and remaining Rs 20,000 crore is in the form of foreign loans and bonds. Further, RCom has classified Rs 22,550 crore of borrowings as non-current liabilities.

On the other hand, Rcom's net loss more than doubled to Rs 2,709 crore in Q2FY18 compared to net loss of Rs 1,210 crore in Q1FY18 and net profit of Rs 62 crore in Q2FY17. Also, totol income came in at Rs 2,667 crore in Q2FY18 down by 48.13% year-on-year (YoY) and 25.73% quarter-on-quarter (QoQ) basis.

There are three terms which can explain the company's capability for repaying debt. They are debt-to-equity ratio measuring a company's financial leverage, debt service coverage ratio calculating cash flows available to pay current debt obligations and interest service coverage ratio – which determine how easily a company can pay their interest expenses on outstanding debt.

Data from Rcom financial report, it was known that debt-to-equity ratio of Rcom stood at 1.91 times in 1HFY18 compared to 1.45 times in 1HFY17. While debt and interest service coverage ratio was at 0.02 times and 0.04 times in 1HFY18 as against 0.65 times and 2.33 times respectively in 1HFY17.

During Q2FY18, Rcom in its audit report mentioned that, the monetization of RCOM assets being carried out in a transparent process anchored by SBI Capital Markets Limited is at advanced stage.

HSBC said, “Key upside risks include unlocking value in undersea cable assets and ability to monetize spectrum assets particularly spectrum in the 800, 1800 and 2100 spectrum band. An additional upside risk will be the ability to monetize tower assets.”

Lastly HSBC said “Our revised target price is Rs 12 and implies c23% downside. We retain our Reduce rating as we remain sceptical about the core business given the company’s declining market share and slow progress in improving its balance sheet.”

06:32 PM IST

Sensex, Nifty slip on weak global cues; RCom, Indiabulls Real Estate, Bharti Airtel stocks dip

Sensex, Nifty slip on weak global cues; RCom, Indiabulls Real Estate, Bharti Airtel stocks dip Sensex, Nifty sustain pre-budget rally; RCom, ITI, IndusInd Bank stocks gain

Sensex, Nifty sustain pre-budget rally; RCom, ITI, IndusInd Bank stocks gain NCLAT allows insolvency proceedings against Reliance Communication

NCLAT allows insolvency proceedings against Reliance Communication