HDFC Bank continues to be in good books of investors

Surpassing analysts estimates, HDFC Bank on April 21, reported 18.25% rise in standalone net profit, at Rs 3,990.09 crore compared to Rs 3,374.22 crore in the corresponding period of the previous year.

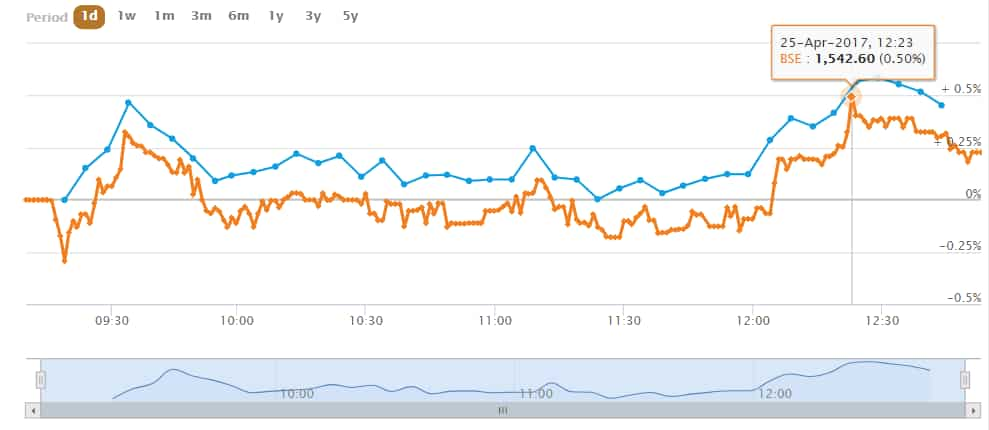

Share price HDFC Bank has touched new highs since it announced its fourth quarter ended March 31, 2017 results

Surpassing analysts estimates, HDFC Bank on April 21, reported 18.25% rise in standalone net profit, at Rs 3,990.09 crore compared to Rs 3,374.22 crore in the corresponding period of the previous year.

HDFC Bank's profitability, coupled with good loan growth, strong cost control, improvement in margins and asset quality has made analysts quite optimistic on the stock.

On Tuesday, share price of HDFC Bank touched an all-time high of Rs 1,542.75 per piece. At 1243 hours, the bank was trading at Rs 1540 per share, up Rs 7 or 0.47%.

Share price of HDFC Bank has been rising for five consecutive days.

In these five days, share price of HDFC Bank has risen by Rs 94 or 6.47%.

Market capitalisation of HDFC Bank has grown by Rs 25,503.38 crore within these five days. Present market cap of HDFC Bank on BSE is Rs 3,94,632.04 crore compared to Rs 3,69,128.66 crore on April 19, 2017.

With this stellar stock performance, HDFC Bank has now risen over 41% in one year. On this day of last year, the shares of HDFC Bank were near Rs 1093 per share level.

Clyton Fernandes analysts at Systematix Institutional Equities said, “We expect an improvement in HDFCB’s valuations going forward, aided by robust core earnings and strong capital adequacy. We expect it to be the best placed among peers in managing near-term challenges of capital adequacy (Basel 3 norms), liquidity coverage and credit quality.”

While Manish Agarwalla, Pradeep Agrawal, Paresh Jain analysts at Phillip Capital said, "HDFC bank has managed to outperform the system loan growth with a huge margin. Loan book picked up once the effects of demonetisation faded and is expected to continue 20% CAGR over next few years. CASA accretion gained momentum due to surge in deposit. NIMs are likely to remain stable at 4.3% due to decline in cost of funds and increasing share of higher yielding assets."

This Q4, loan growth stood at Rs 5.55 lakh crore, rising by 19% year-on-year (YoY) and 12% quarter-on-quarter QoQ basis. Incremental growth in the quarter was driven by corporate loans which accounted for 62% incremental share; 36% of overall loans.

Systematix said, "The strong growth in corporate despite unfavorable market condition is driven by shifting of credit substitutes like CPs to loan book given steep cut in MCLR across the industry."

Moreover, total deposits was over Rs 6.43 lakh crore in Q4, witnessing rise of 17.8% yoy and 1.4% qoq.

The trio said, "Digital initiative started paying off with cost on establishment and branch addition moderating. Cost to income ratio to show gradual improvement. Overall asset quality continues to remain stable. Subsidiary had reached decent size and expected listing of HDB financial will unlock value of the entity."

Further the trio added, "At current market price, the core book trades at 3.8x/3.2x FY18/FY19 BVPS of Rs375/Rs439 (net of investment in subsidiary), thus valuing subsidiary at Rs75/Rs88 per share for FY18/19. Given HDFC Bank’s strong earnings visibility and superior asset quality we maintain Buy with a revised PT of Rs 1,730 (previous 1,435), which is 3.75x FY19 core book of Rs 439 per share."

Analysts at Motilal Oswal, "HDFC Bank is well positioned in the current environment, With tier 1 capital, strong capacity amid the moderate growth cycle and significant digitization initiatives, the bank is well placed to benefit from the expected pick-up in the economic growth cycle."

However, Fernandes warned on some risks saying, "Slower-than-expected economic growth could impact business growth and asset quality; market share loss to close peers in high-yielding retail loans due to disruptive/competitive strategies."

01:00 PM IST

Exclusive! To fight coronavirus, we should not be dependent only on government: Aditya Puri, MD, HDFC Bank

Exclusive! To fight coronavirus, we should not be dependent only on government: Aditya Puri, MD, HDFC Bank HDFC Bank voted 'Best Managed', 'Best Governed' in India

HDFC Bank voted 'Best Managed', 'Best Governed' in India Cabinet approves Yes Bank restructuring scheme, SBI to take 49 pct stake; Axis Bank, HDFC Bank to invest too

Cabinet approves Yes Bank restructuring scheme, SBI to take 49 pct stake; Axis Bank, HDFC Bank to invest too Maruti Suzuki partners with HDB Financial Services to facilitate easy car loans for customers

Maruti Suzuki partners with HDB Financial Services to facilitate easy car loans for customers Make money from HDFC Bank share price! Experts tip says it can give big returns in just 1-to-3 months

Make money from HDFC Bank share price! Experts tip says it can give big returns in just 1-to-3 months