10 factors that will impact RBI’s decision in first monetary policy review 2018-19

The six-member Monetary Policy Committee including the RBI governor Urjit Patel held a meeting on Wednesday for discussing the policy, and on April 05 i.e is tomorrow, the resolution of the meet will be announced for all.

RBI monetary policy review 2018-19: The Reserve Bank of India (RBI) is just few hours away from presenting the first monetary policy of the fiscal year FY19, and many economists have already projected a status quo in this review for the third time in a row. RBI kept policy repo rate unchanged at 6% since past three monetary policy meetings along with accommodative stance due to fear of higher inflation and macro-economic data.

The six-member Monetary Policy Committee including the RBI governor Urjit Patel held a meeting on Wednesday for discussing the policy, and on April 05 i.e is tomorrow, the resolution of the meet will be announced for all.

Here’s a list of ten factors, that will impact RBI’s decision in this monetary policy, as per Care Ratings.

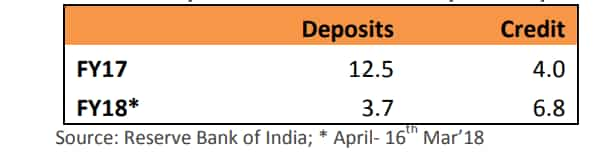

Bank Deposits

For the period April – 16th Mar’18, deposits at Rs 111.61 lakh crore grew by 3.7% lower than 12.5% growth witnessed in the corresponding period last year. This can be ascribed to households migrating from deposits to mutual funds on account of better returns in the market.

In addition to this, last year numbers include the impact of demonetization where the deposit inflows had increased sharply.

Bank credit

Bank credit at Rs 83.77 lakh crore grew by 6.8% during Apr-16th Mar’18 higher than the 4% growth in the corresponding period last year.

Growth was primarily driven by retail segment which increased by 14.5% during Apr- 16th Feb’18. However, growth in manufacturing declined by (-) 2% with medium and large enterprises witnessing negative growth and small and micro enterprises growing by mere 0.2%.

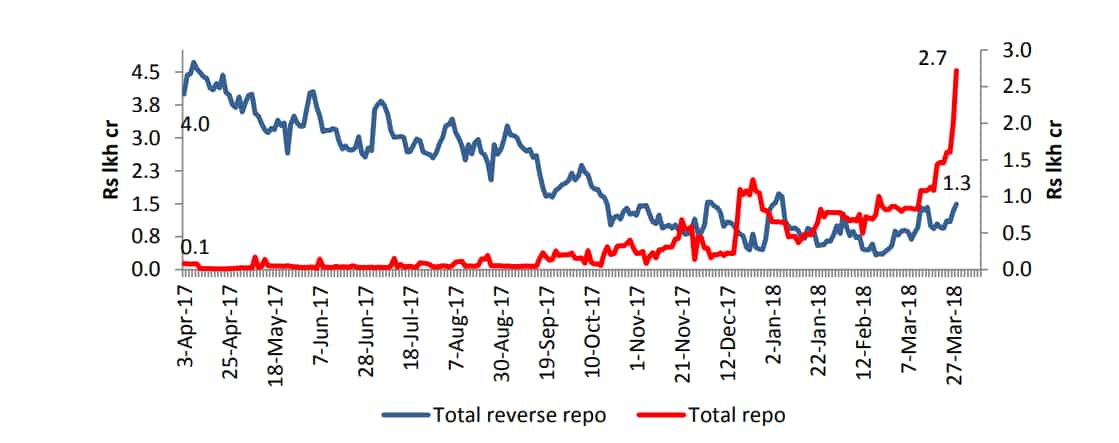

Liquidity Surplus

Substantial liquidity which flowed through the deposits surge post demonetization had gotten absorbed over time. Currently, outstanding funds in reverse repo are around Rs 1.5 lakh crore while o/s repo is around 2.7 lakh crore. Hence, there is a liquidity deficit of Rs 1.2 lakh crore. During the course of the year the RBI has sold securities of almost Rs 90,000 cr through its OMOs.

Interestingly, th government had budgeted market borrowings at Rs 6.05 lakh crore in FY19 higher than Rs 5.99 lakh as per FY18 (RE). Of this total Rs 6.05 lakh crore, government is expected to borrow Rs 2.88 lkh cr in the first half of FY19. This is however, lower than the normal trend given the tight liquidity conditions and high yields.

Consumer Price Index (CPI) Inflation

CPI inflation in Feb’18 at 4.4% eased from a month ago level of 5.07%. This was contained mainly due to food items which grew by 3.3%.

source: tradingeconomics.com

However, inflation in non-food items including fuel, housing and clothing and footwear continue to remain high. Also, RBI has estimated CPI to average 5.1-5.6% in 1HFY19 during last fiscal.

This is a signal that interest rates may not be eased this year and that there could be an increase.

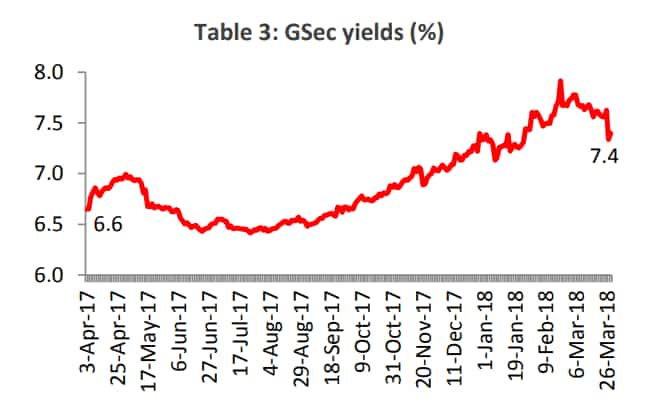

GSec yields

The yields have increased from 6.6% on 3rd April’17 to 7.4% in 28th March’18.

The yields are expected to harden as higher demand for credit from farmers, industry and retail segment in second half of FY19 could pressurize liquidity further.

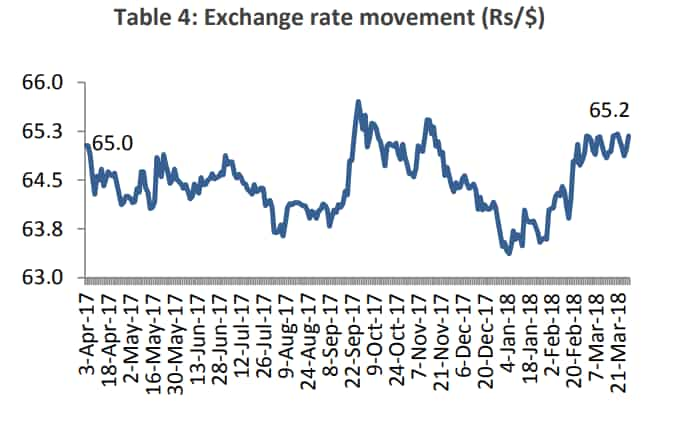

Exchange rate

The rupee strengthened against US dollar in the first half of Jan’18 supported by overseas weakening of the dollar and higher FII inflows. However, the domestic currency depreciated in the month of Feb on lingering concerns over widening fiscal deficit & trade deficit and higher inflation, followed by further depreciation against USD in March month, due to concerns over fiscal slippages and potential global trade war.

Some of the other factors are:

Gross Domestic Product (GDP)

India's Gross Domestic Product (GDP) came in at 7.2% in third quarter October - December 2017 (Q3FY18) - higher compared to 6.3% in Q2FY18 and 5.7%. India's GDP has reached to one-year high, as the last time, the economy stood near 7% mark, was in the corresponding period of the previous year.

source: tradingeconomics.com

The CSO also released second advance estimate numbers for the entire fiscal year FY18.

As per the CSO, the growth in GDP during 2017-18 is estimated at 6.6% as compared to the growth rate of 7.1% in 2016-17.

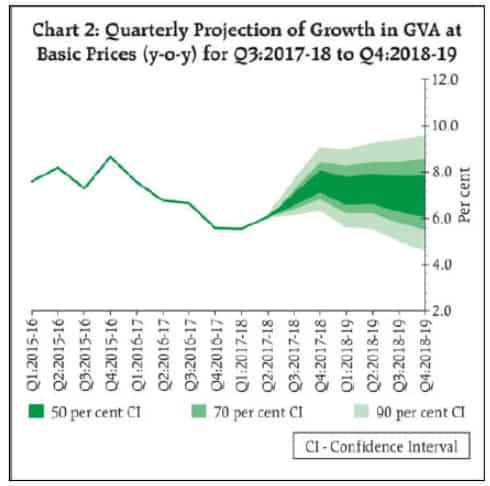

Gross Value Added (GVA)

GVA at basic prices at constant (2011-12) prices in Q3 of 2017-18 is estimated at Rs 30.11 lakh crore, as against Rs 28.21 lakh crore in Q3 of 2016-17, showing a growth rate of 6.7%.

The CSO has anticipated growth of real GVA at basic prices in 2017-18 is 6.4% as against 7.1% in 2016-17.

In last policy, the RBI projected GVA growth for 2018-19 is projected at 7.2% overall – in the range of 7.3-7.4% in H1 and 7.1-7.2% in H2 – with risks evenly balanced.

Wholesale Price Index (WPI) inflation

The Wholesale Price Index (WPI) slightly eased to 2.48% (provisional) in February from 2.84% (provisional) in January.

source: tradingeconomics.com

During February last year, it was 5.51%. Build up inflation rate in the financial year so far was 2.30% compared to build up rate of 4.92% in the corresponding period of the previous year.

Index of Industrial Production

Index of Industrial Production (IIP) or factory output for the month of December 2017 came in at 7.1%, compared to 8.4% in November 2017 and 2.2% in the month of October 2017.

source: tradingeconomics.com

Cumulative growth of IIP for the period April-December 2017 over the corresponding period of the previous year stands at 3.7%.

Thus economists at CARE said, “Given these considerations, RBI is likely to maintain an unchanged stance on policy rates. The important issue will be the tone of the policy- will it be hawkish or neutral. We would tend to think that there would be more than neutral indications with a tint of hawkishness.”

07:41 PM IST

EMI calculation: Should you pay or not? Anil Singhvi explains what home loan, auto loan, other borrowers should do

EMI calculation: Should you pay or not? Anil Singhvi explains what home loan, auto loan, other borrowers should do EMI Moratorium Latest News: What it is? What it means for car, home and other loans? Should you postpone payment or keep paying? Check best advice for you

EMI Moratorium Latest News: What it is? What it means for car, home and other loans? Should you postpone payment or keep paying? Check best advice for you Took home loan, car loan from this bank? Good news for you - Check details

Took home loan, car loan from this bank? Good news for you - Check details SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers

SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers RBI steps will ease pressure on the financial system: Amitabh Chaudhry, Axis Bank

RBI steps will ease pressure on the financial system: Amitabh Chaudhry, Axis Bank