7th Pay Commission: Central government employees, invest 10% of your basic salary plus DA in NPS, become crorepati

What government has done is that it has announced a host of tax exemptions levied under NPS which will help these employees make hefty money on their contributions. The benefits are so big that, if they look closely, central government employees can actually become crorepati.

7th Pay Commission: In the midst of many disappointments suffered by central government employees there are some critical things they should note. The government has finally made some positive moves, even though it is still evading taking action on hike of minimum pay scale and fitment factor under 7th Pay Commission. It is encouraging employees to opt for the National Pension Scheme (NPS). which is seen bringing major relief to them. What government has done is that it has announced a host of tax exemptions levied under NPS which will help these employees make hefty money on their contributions. The benefits are so big that, if they look closely, central government employees can actually become crorepati.

Here’s how central government employees under 7th pay commission can become crorepati. Firstly, it needs to be noted that NPS works on defined contribution basis and will have two tiers - Tier-I and II. Contribution to Tier-I is mandatory for all Government servants joining Government service on or after 1-1-2004 (except the armed forces in the first stage), whereas Tier-II will be optional and at the discretion of Government servants.

In Tier-I, a Government servant will have to make a contribution of 10% of his basic pay plus DA, which will be deducted from his salary bill every month by the PAO concerned. The Government will make an equal matching contribution. However, there will be no contribution from the Government in respect of individuals who are not Government employees.

Tier-I contributions (and the investment returns) will be kept in a limited partial withdraw-able Pension Tier-I Account. Tier-II contributions will be kept in a separate account that will be withdraw-able at the option of the Government servant. Government will not make any contribution to Tier-II account.

Coming to Tier I, Centre will now contribute 14% of basic salary to their pension corpus compared to previous 10%. Apart from this, the employees will continue to give 10% of their basic salary - which leads to overall 24% contribution towards pension. Apart from this, the government has exempted 40% of the withdrawal amount from taxes compared to previous 20%.

It needs to be noted that, already 40% the pension wealth under NPS is compulsory for opting annuity plan. It would be remaining 60% which will have 40% tax exemption.

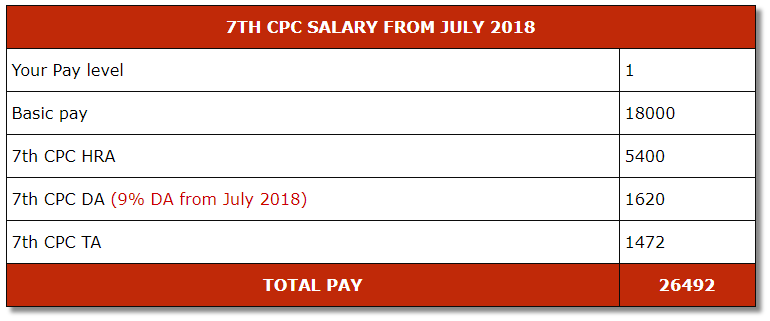

So for instance, if your basic salary is Rs 18,000 per month in level 1 pay scale of 7CPC, then if you contribute 10% of your salary which would be Rs 1,800 along with Dearness allowance (9% from July 2018) of Rs 1,620, then you make total contribution of Rs 3,420 in tier 1 account of NPS.

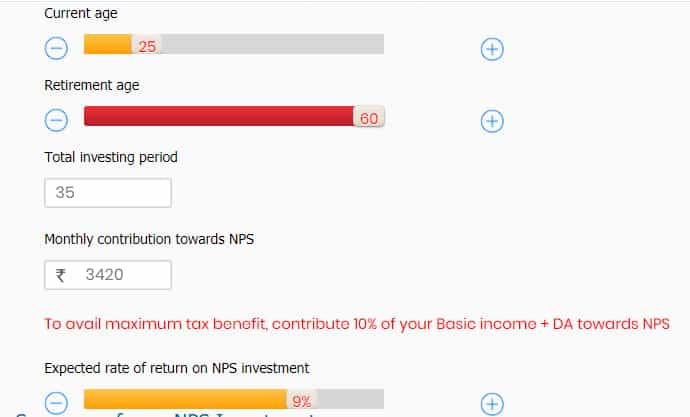

Now if you begin this investment at the age of 25 or earliest as possible, then you pay Rs 3,420 per month for next 35 years, then your overall contribution comes at Rs 14.36 lakh. On this investment, your interest earned is massive Rs 85.31 lakh taking overall pension wealth nearly at Rs 1 crore. The interest rate of NPS is projected at 9%.

(Image Source: SBI Pension Funds calculator)

If 40% of the pension wealth which comes at Rs 39.86 lakh, gets invested in annuity then remaining Rs 59.80 lakh you can withdraw. The amount invested in annuity will give you over Rs 26,000 per month pension after retirement age of 60.

On the remaining Rs 59.80 lakh lump sum withdrawal your 40% is tax exempted.

(Image Source: SBI Pension Funds calculator)

And surprisingly, if you want even further tax exemption then you need to know about three sections namely 80CCD(1), 80CCD(2) and 80CCD(1B).

Section 80CCD(1)!

Under this, an employee’s contribution of 10% plus DA allowance will get up to Rs 1.5 lakh eligible for tax exemption. Such contribution is along with section 80C which also gives similar tax benefit.

Section 80CCD(2)

This one is meant for the employer’s contribution where 10% on basic salary plus DA, will get tax exemption of Rs 1.5 lakh. This is also additional benefit and is not a part of section 80C where Rs 1.5 lakh is exempted.

This section helps employer to claim tax benefit for their contribution which can be shown as business expensive in their profit and loss account.

However, any self employed cannot claim any benefit under this section.

Section 80CCD(1B)

Introduced since Budget 2015-16, this allows an employee to avail tax deduction on additional contribution made under NPS. Up to Rs 50,000 extra contribution made apart from 10% basic salary plus DA allowance, has a tax exemption under section 80CCD(1B). This is also not part of claims offered under section 80C.

For example, Prakash is an government employee and his employer deducts Rs 70,000 per annum (includes 10% basic salary plus DA) from his salary as a part of contribution in NPS. Similarly, employer also makes its share of contribution. Under which section Prakash should claim tax benefit?

It needs to be noted that, employer will only claim tax benefit under section 80CCD(2). As for Prakash has an option between section 80CCD(1) and section 80CCD(1B). He can either show Rs 50,000 as an investment under section 80CCD(1B), and remaining Rs 20,000 can be claimed under section 80CCD(1). Also one should note that 80CCD(1) along with Section 80C has investment limit eligible for tax deduction as Rs 1.5 lakhs.

Thereby, Prakash should make an additional Rs 1.30 lakh in section 80C to claim maximum benefit. Overall, a person can avail Rs 2 lakh tax benefit.

Similar is the case when your NPS contribution is above Rs 2.1 lakh, one can claim tax benefit under section 80CCD(1B) and section 80C, section 80CCD(1).

Hence, central government employees under 7th pay commission aegis, what are you waiting for, get richer than before! Make most of NPS scheme, and retire a crorepati.

02:57 PM IST

7th Pay Commission Sarkari jobs: Bumper Rs 5,500 monthly salary hike for these employees; Level-9 grade pay after promotion

7th Pay Commission Sarkari jobs: Bumper Rs 5,500 monthly salary hike for these employees; Level-9 grade pay after promotion 7th Pay Commission Latest News: Sarkari jobs at FSI; 13 posts announced with attractive pay as per 7th CPC

7th Pay Commission Latest News: Sarkari jobs at FSI; 13 posts announced with attractive pay as per 7th CPC  7th Pay Commission: Big Coronavirus relief for these Central Government Employees on availing leave

7th Pay Commission: Big Coronavirus relief for these Central Government Employees on availing leave 7th Pay Commission latest news: UPSC notifies 7th CPC Group 'A' Gazetted Officer's job; Rs 56,100 starting salary for this sarkari naukri

7th Pay Commission latest news: UPSC notifies 7th CPC Group 'A' Gazetted Officer's job; Rs 56,100 starting salary for this sarkari naukri 7th Pay Commission Latest News: Sarkari jobs available at this research organisation; attractive pay as per 7th CPC

7th Pay Commission Latest News: Sarkari jobs available at this research organisation; attractive pay as per 7th CPC