Bank credit growth will inch up this year but will still remain weak

Madan Sabnavis and Anuja Shah economists at Care Rating said, “Performance of in FY18 will depend on how the manufacturing sector fares as this is required for revival in growth in bank credit. With a share of above 40%, it is the driving force."

Prime business of banks, i.e. loan disbursement, will rise slightly in the current financial year after falling to a six-decade low.

As per the Reserve Bank of India (RBI's), bank credit growth stood at Rs 76.31 lakh crore for the fortnight of April 14, 2017, rising 5.52% from Rs 72.31 lakh crore in the week to April 15, 2016.

In the financial year end on March 2017, bank's outstanding credit growth reached at Rs 78.81 lakh crore compared Rs 75.01 lakh crore as of April 2016. Thus, credit growth in 2017 stood at 5.08% lowest since 1953-54 when it had inched up by a paltry 1.7%.

Slowdown in the credit growth has been led by banks' stressed and bad loans, stagnant corporate investment environment and some migration to the corporate debt market where interest rates were more elastic to policy rate changes. Also, last five months of FY17 where credit growth reached into negative territory as a byproduct of demonetisation.

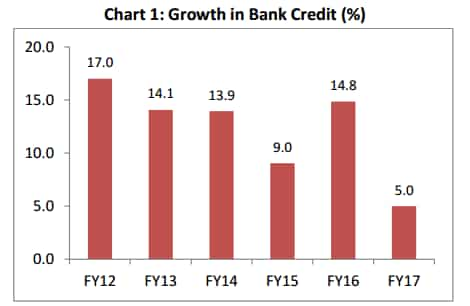

Between FY12 – FY16, credit growth grew in double-digits, barring FY15 where it rose by just 9%.

Compounded annual growth rate (CAGR) was healthy during FY12 – FY16 at 12% slided down to 5% in FY17.

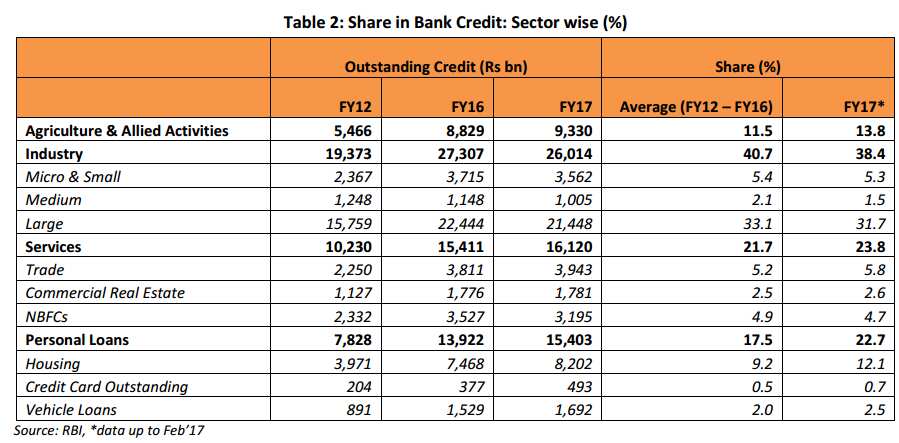

Almost all sectors saw a decline growth rate in credit disbursement FY17 starting with credit to agriculture sector which came down to 5.7% in FY17.

While personal loans managed to suvive at double-digit growth of 10.6% CAGR in FY17, but were lower compared to 15.5% during FY12 – FY16. This double-digit was led by rise in credit card outstanding which grew by a whopping 30.9% in FY17 from 16.5% between FY12-16.

Meanwhile, other categories like housing and vehicle loans saw downward trend of 9.8% and 10.7% in FY17 as against 17.1% and 14.5% between FY12-16.

Service credit growth also lowered to 4.6% in FY17 versus 10.8% between FY12-16. NBFC under this category witnessed decline of 9.4% in FY17 from 10.9% between FY12-17.

Credit to industry was the lowest performer in FY17 with a negative trend of 4.7% compared to 9% in FY12-16. All three segment namely micro & small, medium and large industry saw negative growth of -4.1%, -12.5% and -4.4% respectively in FY17.

Not only, this share of credit towards industry reduced to 38.4% in FY17 compared to 40.7% from FY12-16. While credit to remaining category saw surger in their share during FY17.

Crisil, in its report said, “We expects bank credit growth to remain muted at 8-10% in fiscal 2018, led by low industrial capital expenditure and continued refinancing through bond markets. Retail sector growth will continue to show higher growth as consumption demand gradually picks up and cost of borrowing falls.”

Madan Sabnavis and Anuja Shah economists at Care Rating said, “Performance of in FY18 will depend on how the manufacturing sector fares as this is required for revival in growth in bank credit. With a share of above 40%, it is the driving force."

The duo further added, "With the increase in commodity prices, the absolute demand for loans could come up. With overall GDP growth expected to be only moderately better in FY18. We expect the credit to grow between 7-8% in this fiscal with industrial growth of credit to be around 5-6%.”

Alok Shah, Banking Analyst, Centrum Broking, said, "One of the reasons for moderation in credit growth could be attributed to shift in credit demand towards non-bank channels like corporate bond and commercial papers."

Bonds and Commercial Paper (CP) has emerged as important source of funding for industries, as the flows into key investor segments such as mutual funds and insurance companies remain high. Corporate bond book has been growing at 16-18% year-on-year for the past 12 months in India.

Recently to revive banks credit growth RBI in its minutes of meeting said, "Along with re-balancing liquidity conditions, it will be the Reserve Bank’s endeavor to put the resolution of banks’ stressed assets on a firm footing and create congenial conditions for bank credit to revive and flow to productive sectors of the economy."

01:49 PM IST

Rate cut or status quo: 14 factors will revolve around RBI decision

Rate cut or status quo: 14 factors will revolve around RBI decision Led by Commercial Papers, credit offtake clips 15% to Rs 80.09 lakh crore

Led by Commercial Papers, credit offtake clips 15% to Rs 80.09 lakh crore Can a home loan push help banks revive credit growth?

Can a home loan push help banks revive credit growth?  Will RBI's 25 basis points repo rate cut impact your home loan EMIs?

Will RBI's 25 basis points repo rate cut impact your home loan EMIs? Record low credit growth: 1,000 cos borrowed Rs 1 trillion less in FY17

Record low credit growth: 1,000 cos borrowed Rs 1 trillion less in FY17