Budget FY19 ties RBI’s hand for rate cut in its last FY18 policy

Analysts have already predicted that inflation is going to shoot higher than the RBI’s trajectory for FY18.

After the presentation of Union Budget FY19, the next big thing is the Reserve Bank of India’s last bi-monthly monetary policy announcement for FY18 this week.

The RBI’s decision is keenly awaited for many reasons. The central bank has kept policy repo rate unchanged at 6% in the past two monetary policy meetings along with accommodative stance due to fear of higher inflation and macro-economic data.

In its December policy, RBI highlighted the need to monitor certain variables from the perspective of inflation, which included, rising input cost conditions, pointing towards higher risk of pass-through to inflation; implication of fiscal slippage on inflation; global monetary policy normalization in Advanced Economies and fiscal expansion in the US carrying risks for inflation amongst others.

The Budget 2018 is likely to impact RBI’s outlook.

Beginning with inflation, Anish Damania and Bhawana Chhabra, analysts at IDFC Securities, said, "We think that the Budget is likely inflationary and could lead to some cautious behaviour from the RBI.”

In the Budget FY19, Jaitley announced to raise minimum support price (MSP) for all crops. MSP will be set at 1.5 times of agriculture production cost, and for this the FM proposed to ensure cost plus 50% for all monsoon crops.

There are currently 23 crops supported by MSP. Jaitley also decided to increase food subsidy by 21% or Rs 29,041 crore to Rs 1.69 lakh crore.

While providing relief to farmers, the Finance Minister also decided to increase agriculture credit by 10% to Rs 11 lakh crore.

Now with hike in MSP, it is expected that food price inflation is set to rise ahead.

Consumer Price Index (CPI) inflation has already reached to 17-month high of 5.21% in December 2017, primarily driven by vegetables, house rent and fuel.

source: tradingeconomics.com

Sujan Hajra and Pooja Banthia, economists at Anand Rathi, had earlier stated that the divergence between wholesale and retail inflation is again emerging, reflecting higher food and services inflation along with modest manufactured price inflation.

In December monetary policy, RBI expected inflation in the range of 4.3% to 4.7% in Q3 and Q4 of this year, including the HRA effect of up to 35 basis points with risks evenly balanced.

RBI had said, “First, moderation in inflation excluding food and fuel observed in Q1 of 2017-18 has, by and large, reversed. There is a risk that this upward trajectory may continue in the near-term.”

Analysts, however, have already predicted that inflation is going to shoot higher than the RBI’s trajectory for FY18.

Madhavi Arora, Upasna Bhardwaj and Suvodeep Rakshit, analysts at Kotak Institutional Equities, said, "Adverse base effect continues to propel the CPI inflation readings significantly higher than RBI’s expected range of 4.3-4.7%. CPI inflation trajectory is set to trend even higher towards 5.5-6% in 1QFY19, along with a cyclical economic recovery.”

Analysts at IDFC said, “With so much focus on farm incomes and with MSPs being likely increased, there could be an upward bias for food prices. Further, customs duties in many commodities have increased and this could prove to be a bit inflationary.”

Similar views were also expressed by HDFC Bank Investment Advisory Group saying, “Given the increase in the fiscal deficit numbers as well as the hike in MSPs, RBI’s futures monetary policy stance going forward will be very important from the perspective of fixed income markets.”

Secondly, the 10-year benchmark yield has steadily inched up in the run-up to the Union Budget due to issues panning from higher domestic inflation, fears/expectations of a large supply of papers by the Central government.

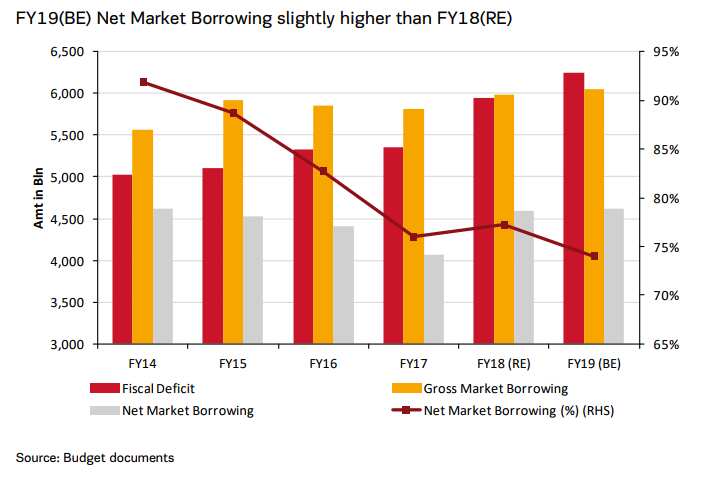

10-year yield which moved to 7.40%-mark on January 29, 2018, reached to 7.60%-level post-budget announcement, despite the government kept net borrowing for FY19BE at Rs 4.62 lakh crore, lower than the most market expectations.

The duo at IDFC stated that this dampened hopes for any support from the RBI via reductions in the benchmark repo rate.

Talking on G-Sec, analysts at Kotak Securities said, “We expect the bond market to remain under pressure in FY2019 amid (1) nearly unchanged net G-Sec supply of Rs 4.62 tn and (2) a slightly adverse outlook on inflation trajectory, especially in 1QFY19, which could risk the start of a rate hike cycle by the RBI.”

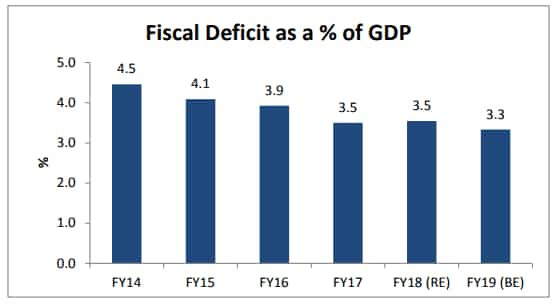

The government’s fiscal deficit target and borrowings will also impact the RBI’s decision. The FM had estimated fiscal deficit target at 3.5% of GDP by end of current fiscal, while the government expects to bring down this target to 3.3% in the next fiscal (FY19).

The Finance Ministry’s target does not match with what analysts are expecting for the country's fiscal position.

In January, Morgan Stanley predicted that India's fiscal deficit to increase 3.5% of GDP in 2018-19, considering the upcoming state elections in 2018, and general election in May 2019, and weak private investment, concerns have emerged over the government's fiscal position.

For nine months of Financial Year 2018, India's fiscal deficit stands at Rs 6,20,949 crore, overshooting the budgeted estimate (BE) target by 113.6%.

The government has estimated Rs 5,46,532 crore of fiscal deficit for FY18 which during the same period of the last year stood negative at 93.9%.

The budget has projected capital expenditure target to grow by 10% in the upcoming fiscal year, higher than the negative 4% growth of 2017-18.

It may be noted that there has been a sustained decline in the ratio from 4.5% in 2013-14 to 3.5% in 2017-18(RE).

According to the RBI's last policy statement, implementation of farm loan waivers by select states, partial rollback of excise duty and VAT in the case of petroleum products, and decrease in revenue on account of reduction in GST rates for several goods and services may result in fiscal slippage with attendant implications for inflation.

IDFC, however, explains that even though gross borrowings for FY19BE are lower than market expectations, T-bill issuance has been taken at a high level for FY18E. This implies supply fears in the market. Further, our expectation of a retail inflation is unlikely to be conducive for any rate cut from the RBI.

Gross Borrowings are budgeted to decline marginally by 1% as the government expected to borrow Rs 6.3 lakh crore in 2018- 19, lower than Rs 6.41 lakh crore borrowed in the last year.

Given the expected trajectory of inflation, IDFC said, "We see the RBI remaining status quo for a significant period going ahead." It cautioned that in the event that global commodity prices (especially oil shocks) increases further, the probability for a tighter monetary policy could also rise.

Besides, RBI's view on its surplus to government will also be awaited in this policy.

Total dividend from the Reserve Bank of India, nationalised banks and financial institutions is estimated to be around Rs 54,817 crore for FY19, slightly lower than the revised estimated of FY18 which is at Rs 51,623 crores.

Earlier, the government had estimated Rs 74,900 crore dividend, the reason behind lowering the target now is due to low dividend from RBI.

"This indicates that the government is expecting that banks will not park too much additional money with RBI with credit demand picking up," analysts said.,

07:35 PM IST

EMI calculation: Should you pay or not? Anil Singhvi explains what home loan, auto loan, other borrowers should do

EMI calculation: Should you pay or not? Anil Singhvi explains what home loan, auto loan, other borrowers should do EMI Moratorium Latest News: What it is? What it means for car, home and other loans? Should you postpone payment or keep paying? Check best advice for you

EMI Moratorium Latest News: What it is? What it means for car, home and other loans? Should you postpone payment or keep paying? Check best advice for you Took home loan, car loan from this bank? Good news for you - Check details

Took home loan, car loan from this bank? Good news for you - Check details SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers

SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers RBI steps will ease pressure on the financial system: Amitabh Chaudhry, Axis Bank

RBI steps will ease pressure on the financial system: Amitabh Chaudhry, Axis Bank