Has NPA recognition by banks post AQR complete or is it just a myth?

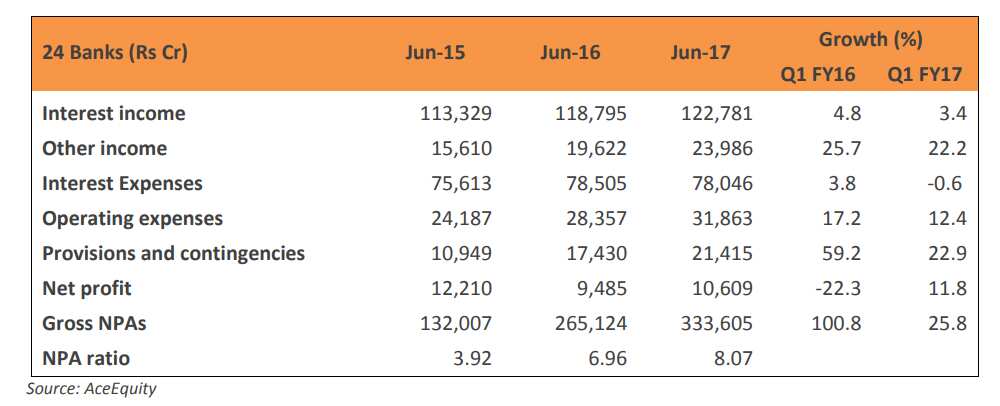

Gross NPAs of 21 banks have reached to 8.07% in June 2017 compared to 6.96% in June 2016 and 3.92% in June 2015.

Key Highlights:

- 21 Banks gross NPAs rose to 8.07% in June 2017

- Provisions grew by 22.9% in Q1FY18

- PSBs three times higher than private banks in gross NPAs during

With the end of Asset Quality Review (AQR) in March 2017, it was expected that recognition of bank's non-performing assets (NPAs) must have been complete – leaving better room for resolution of the problem.

First quarter of fiscal year 2017 – 18 (Q1FY18) has begun and a list of 24 banks (10 public sector banks and 14 private banks) have already presented their financial performance.

Banks have conducted the AQR between August 2016 and March 2017 where they were asked to recognise three kinds of loans which included NPAs, restructured loans and projects that did not begin on time.

During Q1FY18, gross NPAs of these banks in value term rose by 25.8% to Rs 3,33,605 crore compared to Rs 2,65,124 crore in the corresponding period. In percentage terms, gross NPAs which stood at 3.92% in June 2015, 6.96% in June 2016 have reached to 8.07% in June 2017.

Care Ratings, in its report said, “Gross NPAs increased at a much lower rate in Q1 FY18 as compared to Q1 FY17 as many banks have been cautious in lending on account of higher stressed assets in the past few quarters.”

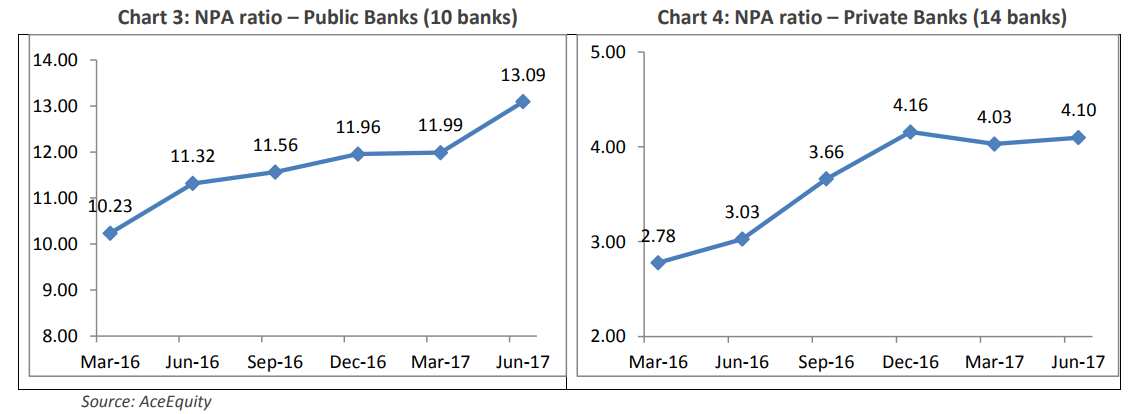

Gross NPA ratio of PSBs are nearly 3 times that of the private banks as on June 2017. NPAs of PSBs are presently at 13.09% while that of private stood at just 4.10% by end of Q1FY18.

Between June 2016 – June 2017, NPAs of PSBs has risen by nearly 2%, while of private banks by just 1%. This indicates that PSBs appear to be more stressed than private banks.

According to Care Ratings, the NPA reconciliation process was to be completed by March 2017; however NPAs continue to be high as of June 2017. This may be on account of two factors – the NPA reconciliation process is still going on and New (incremental) NPAs are still being generated.

The Reserve Bank of India itself thinks that NPAs of banking universe will go up by end of March 2018. On June 30, RBI warned stating that asset quality of banks continued to remain weak with gross non-performing loans rising to 9.6% in the year to March 2017 and may rise to 10.2% by next March.

By end of FY17, banks had gross non-performing assets (NPAs) of 9.5% of gross advances valuing up to Rs 7.65 lakh crore. GNPAs of a total 21 PSBs stood at Rs 6.19 lakh crore, rising by 19.96% compared to Rs 5.16 lakh crore in the similar period of the previous year.

RBI's financial stability report showed that although there is a fall in stressed advances ratio in agriculture, services and retail sectors, the stressed advances ratio in industry sector, however, rose from 22.3% to 23%, mainly on account of sub-sectors such as cement, vehicle, mining & quarrying and basic metals.

“The stress test indicated that under the baseline scenario, the average GNPA ratio of all commercial banks may increase from 9.6% in March 2017 to 10.2% by March 2018,” added the report.

India Ratings earlier stated that banks have been sitting on unrecognised stressed loans worth Rs 7.7 lakh crore including both corporates and SME debt – which holds 22% of total bank credit.

It expects impaired assets to peak at 12.5%-13% by FY18/FY19 while credit costs will show an extended recovery period as a large proportion of the recently acquired higher–bucket non-performing loans keep aging.

At the same time, provisions also increased but at lower rate. Q1FY18 saw provisions of Rs 21,415 crore, increasing by 22.9% compared to Rs 17,430 crore a year ago same period. This is lower compared to 59.2% rise in Q1FY16 provisions from Rs 10,949 crore in Q1FY15.

Clyton Fernandes Vice President - Institutional Research, Systematix said, "We expect asset quality issues for the sector to have continued, given the persistent weak macro-economic environment, leading to further provisioning for NPAs arising from restructured loans and for fresh slippages. Thus, we expect credit costs to remain high for most banks, though lower yoy."

ALSO READ:

01:06 PM IST

Disclose names of defaulters, suggests parliamentary panel

Disclose names of defaulters, suggests parliamentary panel Punjab National Bank, Union Bank bad loan growth slows but provisions weigh

Punjab National Bank, Union Bank bad loan growth slows but provisions weigh Jaitley likely to hold meeting with bankers on Nov 11-12

Jaitley likely to hold meeting with bankers on Nov 11-12 Q2FY18 preview: RBI's NPA resolution under IBC to weigh on banks' earnings

Q2FY18 preview: RBI's NPA resolution under IBC to weigh on banks' earnings  Fewer and stronger PSU banks but what about their stressed assets?

Fewer and stronger PSU banks but what about their stressed assets?