How to get PMAY subsidy on home loan and are you eligible for it?

Earlier, the PMAY scheme was meant for rural poor for whom loan provision was from Rs 3 lakh to Rs 6 lakh. Now, the scheme has been extended to the urban poor and urban middle class too. Also, the loan provision has been extended up to Rs 18 lakh.

Planning to buy your dream home! Pradhan Mantri Aawas Yojna (PMAY) can be a better option provided you know the eligibility criteria and some basic information like how to claim the benefit of this scheme. Earlier, the scheme was meant for rural poor for whom loan provision was from Rs 3 lakh to Rs 6 lakh. Now, the scheme has been extended to the urban poor and urban middle class too. Also, the loan provision has been extended up to Rs 18 lakh. But, the scheme has some terms and conditions which the public in general must know before claiming its subsidy and other benefits. Under new norms, the GST levied on the home buyers is 8 per cent while for home buyers not into the PMAY Scheme have to pay 12 per cent GST. For this, the claimant must apply for home loan under Credit Linked Subside Scheme (CLSS) that makes you eligible for the PMAY subsidy.

INCOME TAX SLAB

If you are trying to take the benefit of PMAY, first you must know the income tax bracket in which you fall in. From January 1, 2017 the terms and conditions were changed by the government of India. Now, people earning less than Rs 3 lakh per annum would fall under the Economically Weaker Section (EWS). A claimant under the EWS category can avail maximum subsidy provided he or she has supportive documents in this regard. People falling in the income bracket of Rs 3 lakh to Rs 6 lakh are categorised into Light Income Group (LIG). Similarly, people earning above Rs 6 lakh but below Rs 12 lakh are categorised as Middle Income Group 1 (MIG 1) and people having income below Rs 18 lakh and above Rs 12 lakh are under the MIG 2 category.

Remember, in all categories, one need to submit documents in regard to their income claims verified by the proper authority. For common understanding, best proof of your income is the ITR, irrespective of the fact whether you fall into the list of income tax payee or not.

See Zee Business Video below:

ग्रेफाइट के शेयरों में इसी महीने दिखी करीब 30-35% की गिरावट, क्यों आई ग्रेफाइट इंडिया में तेज़ गिरावट, जानिए वजह सुमित मेहरोत्रा से।@AnilSinghviZEE @SumitResearch @deepaliranaa pic.twitter.com/3BNRhDpkWp

— Zee Business (@ZeeBusiness) January 28, 2019

RATE OF INTEREST

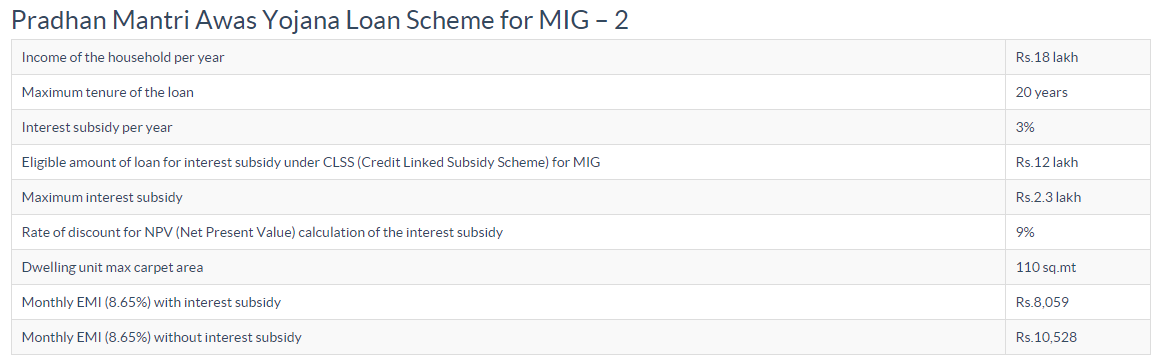

As per Housing and Urban Development Ministry's guidelines updated on January 1, 2017 people earning up to Rs 18 lakh but below Rs 12 lakh or or falling under the MIG 2 category can get home construction loan up to Rs 12 lakh and will get interest subsidy of 3 per cent. In this category, the loan has to be repaid in maximum 20 years time. If a person decided to repay the Rs 12 lakh loan in 20 years, he or she would get an interest benefit of Rs 2.3 lakh that the Indian government would pay on behalf of the home buyer. For this category, the carpet area should not be more than 110 sq. mtrs.

For people earning from Rs 6 lakh to Rs 12 lakh, or falling under MIG 1 category, maximum loan allowed is Rs 9 lakh and interest subsidy is 4 per cent. If one decided to repay Rs 9 lakh loan in 20 years, he or she would get around Rs 2.39 lakh interest subsidy. For MIG 1 category, carpet are should not be more than 90 sq. mtrs.

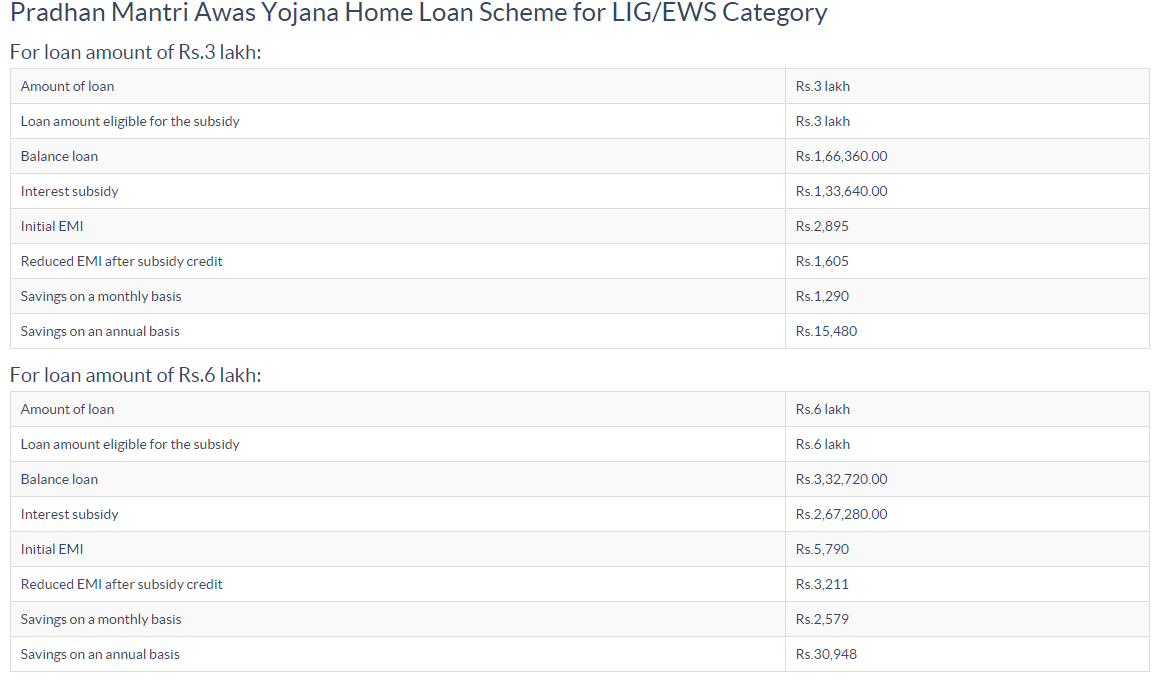

For LIG category people, maximum loan allowed is Rs 6 lakh for a maximum period of 20 years. LIG category people will get 6.5 per cent interest subsidy leading to savings of around Rs 2.46 lakh in 20 years.

Remember, PMAY subsidy loan are available for construction or repair of a re-sale property too.

Loans are available at all commercial banks, housing finance companies, regional rural banks, state co-operative banks, urban co-operative banks, non banking financial companies etc.

TERMS AND CONDITION

Under PMAY, the Indian government plans to provide one house to each house hold. So, a claimant qualifies for the PMAY scheme if he or she doesn't have any home against his or her name. Those who already have a house can'claim for the PMAY subsidy. A claimant needs to give details of his or her family along with the Aadhar Card of each family member. If any of the family member (husband, wife, son and unmarried daughter) has availed any housing scheme of the Indian government before, his or her PMAY subsidy claim would be rejected. Both husband and wife can't claim for the PMAY subsidy but married daughter(s) an son(s) can claim as married child is considered as separate family.

03:57 PM IST

portal") PMAY: Check eligibility, calculate subsidy amount from this direct link of Pradhan Mantri Awas Yojana (Urban) portal

PMAY: Check eligibility, calculate subsidy amount from this direct link of Pradhan Mantri Awas Yojana (Urban) portal PMAY big milestone! One crore homes delivered under Pradhan Mantri Awas Yojana - Urban category, says NAREDCO

PMAY big milestone! One crore homes delivered under Pradhan Mantri Awas Yojana - Urban category, says NAREDCO PMAY: Momentous achievement for Modi government's flagship mission - Over 1 crore homes sanctioned!

PMAY: Momentous achievement for Modi government's flagship mission - Over 1 crore homes sanctioned!  Budget 2019 expectations: 'Government should increase the threshold value of affordable housing from Rs 45 lakh to Rs 75 lakh'

Budget 2019 expectations: 'Government should increase the threshold value of affordable housing from Rs 45 lakh to Rs 75 lakh'  PM Awaas Yojana: Government plans to construct 60 lakh houses in current year

PM Awaas Yojana: Government plans to construct 60 lakh houses in current year