India Inc's capital expenditure revival still four years away?

Capex by both private and public sector entities, primarily on maintenance will marginally increase in the near term- somewhat Rs 1 lakh crore between FY18 - 20.

Even as the government has taken a few bold steps to revive and reform the Indian economy, quite a few deeper issues remain that is hampering the industries growth.

An India Ratings study said that private sector capital expenditure is likely to grow by Rs 1 lakh crore between FY18 – FY20 due to weak domestic consumption demand, global overcapacity and also negative impact while shifting to GST transmission on working capital.

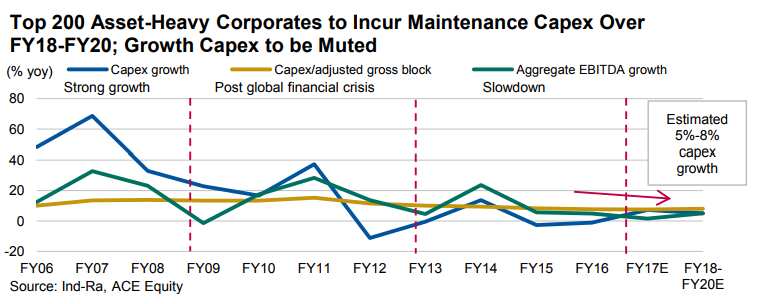

Such capex growth would be a compounded annual growth rate (CAGR) of 5% - 8% in FY18-FY20. This is however better than the CAGR of 4% in FY13 – FY17 but way lower than CAGR of 13% in FY09 – FY12 and CAGR of 49% in FY05-08.

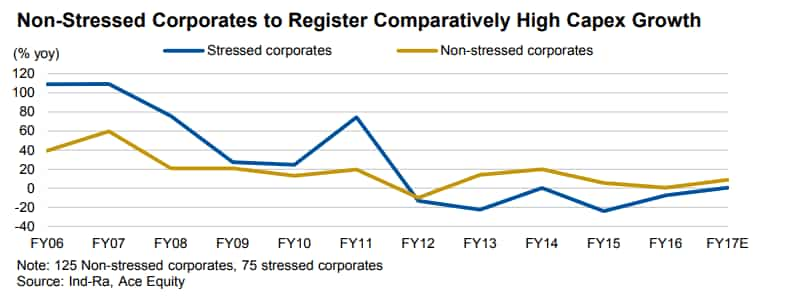

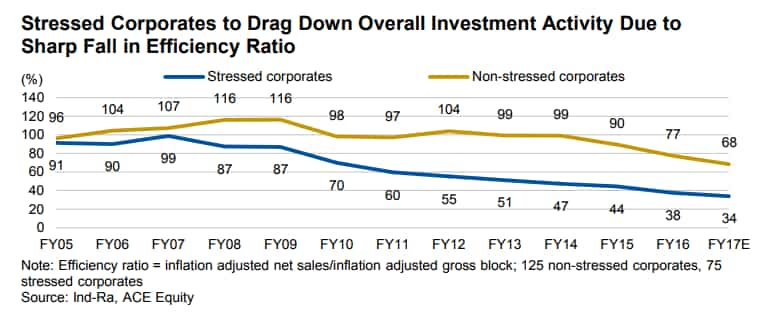

Ind-Ra believes the capex would be largely in the form of maintenance and essential upgrades by the 125 non-stressed corporates of the top 200 asset-heavy corporates. Meanwhile, 75 stressed corporates may face difficulties in even undertaking maintenance capex.

Of these 75 stressed ones, 25 benefit from sponsor support and thus can at least incur maintenance capex.

Analysts at Ind-Ra said, “Although capex by both private and public sector entities, primarily on maintenance, will marginally increase in the near term, a complete turnaround in the investment cycle is unlikely in the next three-four years, until there is high demand visibility and significant deleveraging.”

They added, “Even if investment demand picks up, there would be credit supply constraints with regard to providing fresh credit to corporates by the banking sector owing to risk aversion and higher recapitalisation needs.”

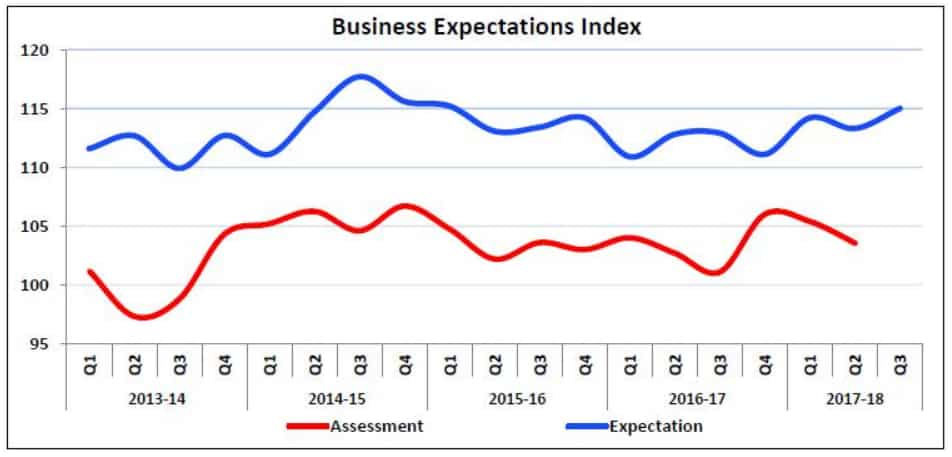

Industry outlook survey for Q2FY18 by the Reserve Bank of India (RBI) showed that the respondents were more optimistic in Q217-18 on the parameters like pending order, exports, imports, and employment; and were less optimistic in case of order books, raw material inventory, finished goods inventory, and overall business situation.

125 non-stressed corporates on account of their strong financial profiles have contributed 80% of total capex in FY17 - while 75 stressed corporates contributed remaining 20%.

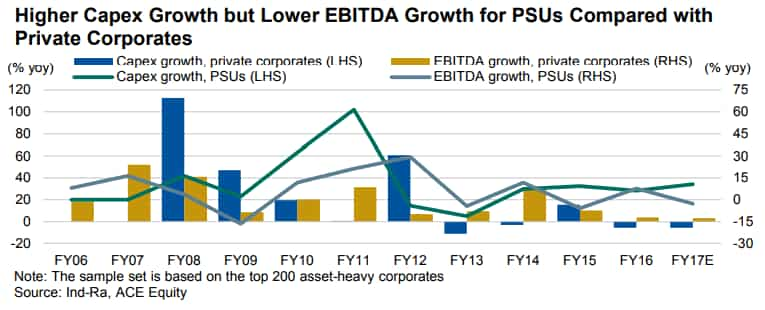

Of the 200 corporates, 50 are PSUs – who accounted for nearly 30% of the capex spending and 37% of adjusted gross block in FY17 (FY06: 46%, 63%). PSUs’ capex rose at a CAGR of 7% over FY12-FY17. However, their EBITDA marginally increased at a CAGR of 1% during the period.

Ind-Ra expects that the high leverage and low operating profitability (EBITDA) levels of the majority of large-scale capex spenders may restrict meaningful capex spending.

Top five asset-heavy sectors namely infrastructure and construction, metals and mining, power, telecom, and, oil and gas accounted for 80% of the adjusted gross block and 75% of

the annual capex in FY17.

These sectors capacity utilisation were muted across FY15-FY17.

Ind-Ra believes there are pockets of stress within sectors, especially infrastructure, metals and power (thermal) owing to high leverage and weak cash flow, limiting their ability to incur large-scale, debt funded capex.

However, their debt levels have peaked and are unlikely to increase from current levels (FY16: 7%; FY17E-FY18E: 4%-8%).

Yet profitability of these corporates is unlikely to significantly improve in the near term (FY16: 5%; FY17E-FY18E: 2%-8%) owing to the weak pace of nominal growth recovery.

Cash flow stress is also to remain elevated leading to weaker balance sheets of stressed corporates, thus indicating their reduced ability to take incremental debt to fund large scale capex.

"Majority of stressed corporates would require another four-five years to deleverage to a sustainable level of 4x-5x from their current leverage of 9x-10x, provided the economic and financial activity reaches FY09-FY12 levels," added Ind-Ra.

01:10 PM IST

RBI issues new framework for resolution of bad loans

RBI issues new framework for resolution of bad loans Stressed assets: Public sector banks recover Rs 1.2 lakh cr in FY19 under IBC

Stressed assets: Public sector banks recover Rs 1.2 lakh cr in FY19 under IBC Banks recover Rs 40,400 cr from defaulters: RBI report

Banks recover Rs 40,400 cr from defaulters: RBI report Banks, FIs sign pact to fast track resolution of bad loans under consortium lending

Banks, FIs sign pact to fast track resolution of bad loans under consortium lending Banks may sell stressed loan accounts to ARCs in absence of bidders

Banks may sell stressed loan accounts to ARCs in absence of bidders