GDP growth rate at 2 year low; RBI's action in next policy will be keenly watched

India's GDP data for Q4FY17 dropped to a two year low. Now the next trigger would be RBI's action on Indian economy during second monetary policy meet.

Q4FY17 data of India's gross domestic products (GDP) came in as a shock to many analysts as it has unexpectedly plunged to a two year low.

On May 31, 2017, the Central Statistics Office (CSO) announced that India's GDP between January – March 2017 period stood at 6.1% compared to 7% in Q3FY17.

This figure is lowest since December quarter ended in 2014 – when GDP recorded growth of just 6%. Even the current performance of India's GDP is lower than China's growth of 6.9% during Q4FY17.

source: tradingeconomics.com

Also Read: Q4FY17 GDP at 6.1% but some sectors defied demonetisation impact

FM Arun Jaitely on a occasion of completing three years of Modi government, held on Thursday, also spoke about the performance of GDP data.

Putting blame on global scenario for slowdown in India's growth, Jaitley said that past three years have been challenging from global economies. He said that significant impact of global situation on India to remain.

Next big thing that will be keenly watched would be the Reserve Bank of India's take on Indian economy in the second bi-monthly monetary policy which is scheduled on June 07, 2017.

Economists at HDFC Bank said, “Overall, while, we do not expect the RBI to reverse its neutral policy stance based on just Q4 growth data, the MPC is likely to take a note of the distinct slowdown and could sound less hawkish in its commentary in the upcoming policy meeting on 7th June.”

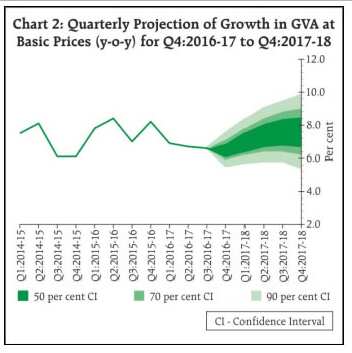

In the first monetary policy which was held on April 06, 2017, RBI had projected GVA growth at 6.7% by end of FY17.

During April policy, RBI projected GVA growth to strengthen to 7.4% in financial year FY18 compared to FY17 with risks evenly balanced.

RBI that time highlighted few points for growth in GVA in FY18. They are - the pace of remonetisation to trigger a rebound in discretionary consumer spending, secondly significant improvement in transmission of past policy rate reductions into banks’ lending rates post demonetisation to help encourage both consumption and investment demand of healthy corporations.

Thirdly, various proposals in the Union Budget should stimulate capital expenditure, rural demand, and social and physical infrastructure, while imminent materialization of structural reforms in the form GST, Insolvency and Bankruptcy Code, and the abolition of the Foreign Investment Promotion Board to boost investor confidence.

Output of GDP is an addition of GVA and taxes minus subsidies on products.

Though GVA growth declined to 5.6%in Q4FY17, if adjusted with the base effect the adjusted GVA growth for Q4 would have been 6.5%, which is 90 basis point higher than the actual number of 5.6% in Q4. For FY17, the adjusted base GVA growth is at 6.8%, compared to the actual of 6.6%.

Urjit Patel governor of RBI along with the MPC members have been categorical that “core inflation is sticky and there are upside risks to inflation from GST, El Nino, Pay Commission and geo political risks” and “Positive growth outlook” even in April.

However, from the inflation numbers and CSO data, growth has been seen on declining trend in FY17. Additionally, inflation risks are now mostly balanced to the downside.

Consumer Price Index (CPI) has reached to a series low at 2.99% in the April 2017 well below market expectations of 3.5%following a 3.81% rise in March.

source: tradingeconomics.com

SBI for FY18 expect CPI inflation to average below 4% with a significant downward bias.

Thus in July policy, SBI expects RBI to maintain the neutral stance but possibly change its perception on inflation to balanced or even downside.

Additionally a widening of the corridor or a signal on the SDF will be a well thought and pragmatic move to push the yields down and ensure monetary policy transmission against the backdrop of significant liquidity overhang in the system, added SBI.

07:20 PM IST

Stock market this week: These factors to drive Indian equity markets

Stock market this week: These factors to drive Indian equity markets When will Indian economy hit $5 trillion mark? Railway Minister Piyush Goyal explains

When will Indian economy hit $5 trillion mark? Railway Minister Piyush Goyal explains Debt market to remain under pressure in April

Debt market to remain under pressure in April India set to grow at 7.2 pc this fiscal on rising consumption: ADB

India set to grow at 7.2 pc this fiscal on rising consumption: ADB India can't achieve 9-10% GDP growth without revolution in farm sector, says Niti Aayog CEO Amitabh Kant

India can't achieve 9-10% GDP growth without revolution in farm sector, says Niti Aayog CEO Amitabh Kant