Investment tips: These 10 stocks can help your wealth grow in July 2019

Considering the month hasn’t begun exciting, it is important to make right and bright investment in order to earn hefty returns.

July 2019 has started on a bittersweet note for Dalal Street, especially post Budget. The day when the final Budget was announced by Finance Minister Nirmala Sitharaman, benchmark indices like Sensex and Nifty once again shot up over 40,000 and 12,000 levels. However, by the time second week started in, investors turned bearish on Indian market, with the Sensex and Nifty struggling to even clock 39,000 and 11,500 levels. On Tuesday, the Sensex finished at 38,730 slightly up by 10.25 points or 0.03%, while Nifty ended at 11,555 below 2.70 points or 0.02%. Stocks like Bajaj Finance, Sun Pharma, Hero Motocorp, LT and Reliance Industries were among gainers.

Interestingly, considering the month hasn’t begun exciting, it is important to make right and bright investment in order to earn hefty returns. But guess what! Karvy Stock Broking analysts in their research note, have listed out 10 stocks which are seen as wealth maximizer on Dalal Street for July 2019. Here’s the list!

(Image source: Karvy Stock Broking)

(Image source: Karvy Stock Broking)

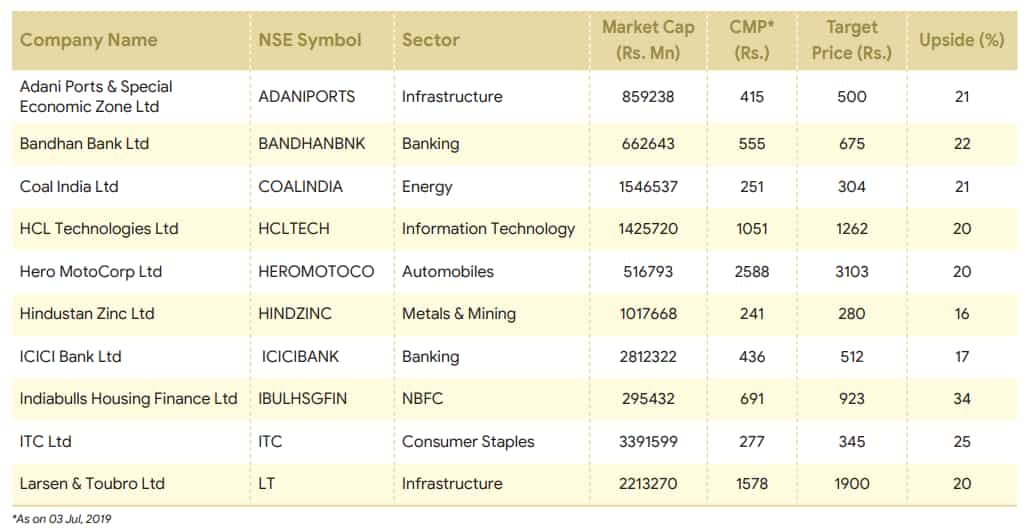

1. Adani Ports & Special Economic Zone Ltd - Healthy growth of container and cargo volumes coming in from the expansion plans are the key positives. Stock is currently trading at 15.8x. The consensus values the company at 19x for a target price of Rs. 500, representing an upside potential of 21%.

2. Bandhan Bank - Bandhan bank is the lowest-cost loan provider in high yield MFI business in East India in a short time and our forecast is on high loan growth in medium term are key positives. Consensus one year target price for Bandhan Bank of Rs. 675 is based on three stage dividend discount model implying 4.3x Mar 21 P/BV. Consensus valuation factors in cost of equity of 12.5%, normalized RoE of 23%, and terminal growth of 6%.

3. Coal India - As per consensus, the stock is valued at a PE of 10.5x of FY21E EPS for a target price of Rs. 304 which gives a potential upside of 21%. The company has to first fulfill its obligation of being able to deliver enough coal to satisfy the growing power needs of the country as coal output has been constrained by delays in obtaining environmental and forest approvals & flexibility is also restricted by socio political factors.

4. HCL Technologies - While the market is disappointed by muted growth guidance and a lower margin guidance, we remain positive on the stock due to its improved organic growth which was a concern till now and upside risks to the overall revenue growth driven by IBM IPs and string order book. The analysts here recommend a “BUY” on HCLT with a price target of Rs. 1262, an upside of 20% based on consensus 1yr forward PE of 14.4x.

5. Hero Motocorp - The stock is currently quoting at 13.4xFY21E earnings. While near term growth outlook for HMCL remains challenging, we remain upbeat on its medium term growth prospects given its competitive advantages like strong brand and distribution network. Also HMCL is in a superior position to benefit from rural economic recovery. It is a debt-free, cash-rich entity with 35%+ average RoE. The analysts have rate “BUY” on the stock for a price target of Rs. 3103 (PER of 16xFY21E).

6. Hindustan Zinc - The company’s lead and silver assets are best in class. The company has strong cash-rich balance sheet. Karvy’s analyst have valued the stock at PE 12.8x of FY21E EPS to reach at consensus TP of Rs. 280 with potential upside of 16%.

7. ICICI Bank - On the back of the new management’s renewed strategy to de-risk the loan book and improving fundamentals, Karvy is positive about ICICI bank and recommend a “BUY” with a price target of Rs. 512, an upside of 17%, based on consensus 1-Yr forward PBV estimate of 2.78x.

8. Indiabulls Housing Finance - IHFL has come a long way from being a diversified lender to a focused mortgage player and now a proposed bank. Its transformation has yielded returns, with RoE improving from 3% in FY09 to 25% in FY19. IHFL’s asset quality remains stable and the bank’s focus on core mortgage loans and its proposal to convert into a bank will drive growth moving forward. IHFL is currently trading at 1.4x P/B on FY20E and based on consensus we assign a “BUY” rating on stock with a TP of Rs. 923.

9. ITC - Long term position of the company remains strong on the back of high market share, high barriers to entry and improving profitability of the non cigarette business. Valuations have been impacted in recent times on account of increasing share of the illegal cigarette business and the company trades at a consensus 1 year forward P/E of 23x, which is below its 5 year average valuation by 8.5% (25.3x). With expectation of stable volumes in cigarettes, and improving performances of the non cigarette businesses, the stock is valued at a P/E of 27.3x on FY21E consensus EPS of 12.64 and recommend “BUY” with a TP of Rs. 345.

10. Larsen & Toubro - L&T’s diversified exposure to various sectors/ geographies coupled with its excellent execution capabilities and its balance sheet strength has resulted in strong order book build up. The consensus values the company at 23x for a target price of Rs. 1900. Delay in capex cycle recovery & order execution may pose a threat to the call.

Also. one advantage of investing at current level is that exchanges and stocks have corrected and are available at affordable price. This makes best stocks a multibagger in near to long term.

06:56 PM IST

Which stocks to buy in August 2019? Experts suggest these 15 shares

Which stocks to buy in August 2019? Experts suggest these 15 shares  Hot stock alert! Buy Mahindra & Mahindra shares now, say experts, Ssangyong and Detroit links are big reasons why

Hot stock alert! Buy Mahindra & Mahindra shares now, say experts, Ssangyong and Detroit links are big reasons why Want to make money on Dalal Street? These 10 stocks can give 14% to 44% returns

Want to make money on Dalal Street? These 10 stocks can give 14% to 44% returns Late, but not too late! From Rallis India to Dhanuka Agritech, Monsoon makes these 5 stocks best bets on D-Street

Late, but not too late! From Rallis India to Dhanuka Agritech, Monsoon makes these 5 stocks best bets on D-Street  How to become rich in India on stock markets: Think beyond large caps, these 12 midcaps are seen skyrocketting

How to become rich in India on stock markets: Think beyond large caps, these 12 midcaps are seen skyrocketting