RBI Rate Hike or Status Quo? 8 big factors that will force Guv Urjit Patel's hands

However, a majority of analysts are predicting that RBI will stick with the status quo in this policy. Some analysts have not ruled out a rate hike either. India's policy repo rate stands at 6.50%.

RBI governor Urjit Patel will be announcing today whether RBI will hike key rates or will it stick to the status quo - no, disappointingly, there is virtually no chance of a rate cut! The 5th bi-monthly monetary policy announcement will happen today at around 1430 hours. This time's policy is quite interesting, as the ongoing battle between RBI and government may somehow have an impact on Patel's decision. Centre wants a rate cut as it is election season and it wants more than adequate liquidity in the system to pump-prime the economy.

However, a majority of analysts are predicting that RBI will stick with the status quo in this policy. Some analysts have not ruled out a rate hike either. India's policy repo rate stands at 6.50%. RBI has maintained a status quo in previous policy surprising every expert. Ahead of policy, Sensex is trading at 35,900.90 - it has plunged 233 points or 0.65%. At the NSE, Nifty 50 was down 83.65 points or 0.77%, trading at 10,785.85 at around 1113 hours.

Coming to today's policy announcement, Rajesh Sharma, MD , Capri Global Capital Limited said, "We expect RBI to hold rates in the Wednesday policy review. Also, we would like them to come up with measures which further boost confidence of Investors and Lenders to NBFCs, which have attracted negative attention in spite of healthy fundamentals."

Similarly, CARE Ratings said, "On the foregoing, we expect that there would not be any rate hike by the RBI in December’18 credit review, nevertheless the stance might change to neutral from calibrated tightening on easing inflationary concerns. We had earlier expected CRR cut by 50 bps in order to pump in liquidity in the banking system. However, as RBI has scaled up OMO purchase operations the chances of CRR cut now appear to be equally balanced (50% probability)."

Now, whether RBI chooses to maintain a status quo or a rate hike, or even shock everyone with a rate cut, will be keenly watched. However, these eight factors will look to force RBI Governor Urjit Patel's hands in decision making as per CARE Ratings.

Banking sector:

The bank deposits have grown by 3.5% between March and November 9th as against 0.7% growth in the comparable period previous year.

Bank credit growth has improved further in the current fiscal. The bank credit off take (y-o-y) as on 9th Nov’18 was at a 5 year high of 14.9%. On an incremental basis (1Apr- 9 th Nov’18), bank credit growth is 5.6% compared with the 0.6% growth in the comparable period in the previous year.

Liquidity position:

Net liquidity in the banking system continued to be deficient on November’18. On an average, the liquidity deficit amounted to Rs. 81,222 crore during 2nd Nov-29th Nov’18.

In order to infuse liquidity in the banking system, the RBI has undertaken OMO purchases of Rs. 1.36 lakh crore.

In December’18, Rs. 40,000 crore liquidity infusions via OMO purchase will be undertaken.

Outcome of RBI Board meeting:

The RBI Central Board discussed 4 subjects in the meeting held on 19th November 2018.

- Basel regulatory capital framework,

- Restructuring scheme for stressed MSMEs,

- Bank health under Prompt Corrective Action (PCA) framework, and,

- Economic Capital Framework (ECF) of RBI.

Out of these, PCA framework and ECF will be referred to committees. With respect to capital framework i.e. CRAR, the decision has been made to retain it at 9% but extend the transition period for implementing the last tranche of 0.625% under the Capital Conservation Buffer (CCB) by one year up to March 31, 2020. For restructuring of stressed standard assets of MSME borrowers the bank will examine the guidelines. The NPA overhand issue and liquidity crunch faced by NBFCs were not discussed in the meeting.

NBFCs’ liquidity issue:

Banks are permitted to raise their exposure to a single NBFC (non-infrastructure financing NBFC) from 10% to 15% until the end of the year.

Till Dec 31, 2018, the government securities equivalent to the incremental credit disbursed by the banks to NBFCs after October 19 will be eligible for Liquidity Coverage Ratio (LCR) requirements. This is in addition to the 13% carve out from Statutory Liquidity Ratio (SLR) norms permitted for use against LCR requirements.

Banks are allowed to provide PCE to bonds issued by non-deposit taking NBFCs and HFCs with at least 3 years of maturity.The bond proceeds should be used only for refinancing of the existing debt of NBFCs.

Exposure of banks to such bonds for each NBFC should be only 1% of capital funds and within 20% aggregate PCE exposure limit.

NBFCs are allowed to sell or securitise loans of maturity more than 5 years, which are being held by them for 6 months than earlier at least 1 year on their books.

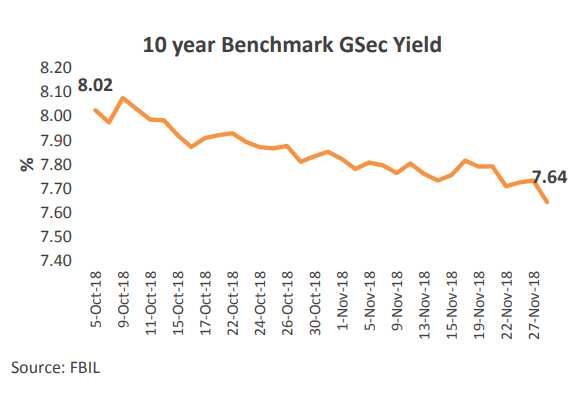

Benchmark GSec yield:

GSec yields saw a declining trend since the last monetary policy yields by 38 bps. This can be attributed to RBI maintaining a status quo on interest rates at its policy meet, the central government reducing its gross borrowing for this fiscal, the OMO purchases undertaken by RBI, easing inflationary concerns and recent appreciation of the rupee.

However, the liquidity deficit in the banking system continues to wield pressure on the yields keeping it above 7.5%.

Since the last monetary policy review in October’18 the base rate has remained constant at an average 9.15% in November’18.

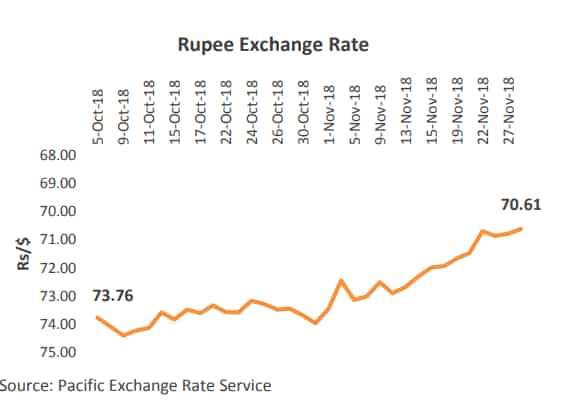

Indian rupee:

The Indian rupee depreciated by 14.1% from the start of the financial year FY19 and touched a low of Rs. 74.4/$ on October 9, 2018.

Thereafter, there has been a trend reversal in the rupee. It appreciated by 5% from Rs. 74.39 per dollar on 9th Oct’18 to Rs. 69.85 per dollar on 29th Nov’18.

Since the last monetary policy, the crude oil prices in the international markets have declined by nearly 30%. Brent oil is around $60 per barrel while WTI is nearly $50 per barrel. The subdued crude oil prices aided the appreciation of the rupee.

FPI investment:

Foreign investors also returned to India in November’18 with foreign investment inflows amounting to $1,664 mn compared with the outflow of $5,104 mn in October’18, which further helped strengthening of the rupee.

Inflation:

The retail inflation has witnessed some moderation in October’18 and came in below 4% target of the RBI aided by benign food inflation with seasonal effect and housing inflation on account of waning statistical effect of HRA implementation under 7th pay commission.

However, it continued to be pressured by high fuel prices owing to rise in crude oil prices globally.

Core inflation continued to remain sticky above 6% mainly due to firm price levels in fuel and transport segment.

Wholesale price inflation rose in October’18 and remained above 5% mark mainly driven by fuel and power prices.

12:20 PM IST

EMI calculation: Should you pay or not? Anil Singhvi explains what home loan, auto loan, other borrowers should do

EMI calculation: Should you pay or not? Anil Singhvi explains what home loan, auto loan, other borrowers should do EMI Moratorium Latest News: What it is? What it means for car, home and other loans? Should you postpone payment or keep paying? Check best advice for you

EMI Moratorium Latest News: What it is? What it means for car, home and other loans? Should you postpone payment or keep paying? Check best advice for you Took home loan, car loan from this bank? Good news for you - Check details

Took home loan, car loan from this bank? Good news for you - Check details SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers

SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers RBI steps will ease pressure on the financial system: Amitabh Chaudhry, Axis Bank

RBI steps will ease pressure on the financial system: Amitabh Chaudhry, Axis Bank