Why small businesses are not willing to go digital

The cost of going digital for small businesses, SMEs and MSMEs are borderline prohibitive. This is the reason why even as the Government is giving incentives for businesses to go digital, some small players are skeptical.

Since November 8, 2016, the focus to shift spending via cash to more digital methods like credit, debit cards, mobile payments, UPIs, net-banking etc are tremendous. On Monday, Ministry of Finance said that small businesses with turnover of Rs 2 crore per year will get special rebate if their gross turnover receipts are received through digital channels.

Ministry said, "In order to achieve the Government’s mission of moving towards a less cash economy and to incentivise small traders / businesses to proactively accept payments by digital means, it has been decided to reduce the existing rate of deemed profit of 8% under section 44AD of the Act to 6% in respect of the amount of total turnover or gross receipts received through banking channel / digital means for the financial year 2016-17. However, the existing rate of deemed profit of 8% referred to in section 44AD of the Act, shall continue to apply in respect of total turnover or gross receipts received in cash."

SMEs work on relatively low margins and higher cost of payments, which in turn puts retailers off the digital payment medium.

MB Mahesh, Nischint Chawathe and Abhijeet Sakhware of Kotak Institutional Equities said, “One of the challenges that we face is our inability to understand the industry in great detail. Unlike a few other developed countries that disclose a lot of studies in the public domain, we are not too aware of the processing costs for the business (charges paid by the retailer) or the MDRs paid.

ALSO READ: RBI lowers MDR charges for up to Rs 2,000 payments via debit card

They added, “The cost of payment through an electronic platform is borne by the retailer whereas any other payment channel is distributed across several stakeholders. Our discussion with various retailers indicates that they work on a PBT margin of 5-7% across various products.”

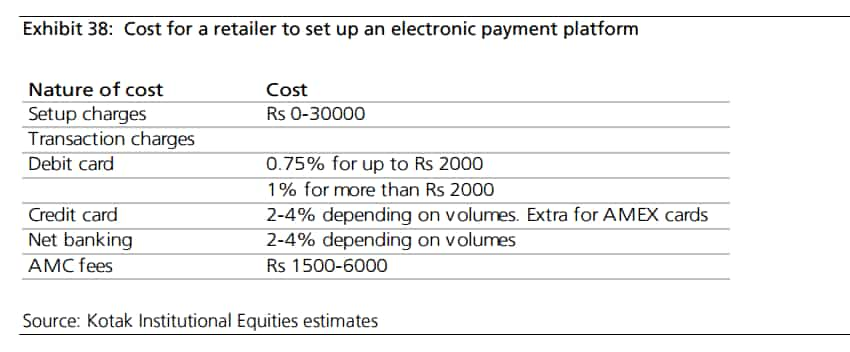

Here are the charges that are borne by a retailer with an electronic payment platforms:

From the above data, it is understood that the cost of the business significantly increases for a small player later resulting in profit erosion.

Even though RBI has decided to relax the cap on MDR by 0.25% for card usage upto Rs 1000 and by 0.50% from Rs 1000-Rs 2000, it is hardly going to be enough.

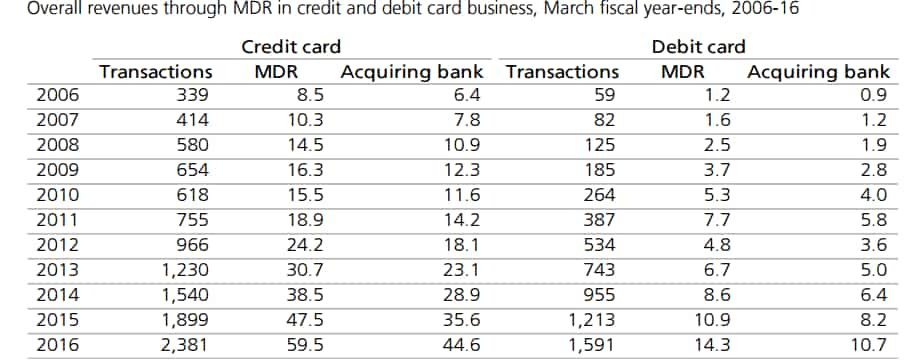

Moreover, the above decision looks like to become beneficiary for credit card usage more compared to that of debit cards.

Kotak assumes that if MDR for a credit card transaction is at 2.5%, then the acquiring bank would be earning 75% of the overall MDR. For debit cards, if MDR is at 0.9%, the earnings is expected to be similar to credit cards.

Till 2012-13, both debit cards and credit cards had similar MDR.

The central bank changed the charges at 0.75% for transactions up to Rs 2000 and 1% above.

Another reason behind SMEs unwillingness towards digital transaction would be the weak tax compliance.

Kotak said, "We believe that one of the most fundamental challenges facing conversion in India is the relatively weak tax compliance prevalent among retailers and customers. The notion that digitally exchanges make for easy scrutiny makes the retailer as well as consumer prefer cash over any other form of electronic payment. "

Apart from it, the additional risk of digital evidence can lead to forced disclosures of higher business income, resulting in further deterioration of earnings profile for the retailer, added Kotak.

05:15 PM IST

Loan disbursement continues to fall post demonetisation, says BFIL

Loan disbursement continues to fall post demonetisation, says BFIL Demonetisation: Steady activation of debit cards to boost ATM volumes for PSBs

Demonetisation: Steady activation of debit cards to boost ATM volumes for PSBs Demonetisation push: Digital payments may grow to $470 billion by 2020

Demonetisation push: Digital payments may grow to $470 billion by 2020 Countless hours lost over demonetisation; parliament sees least productive session in 15 years

Countless hours lost over demonetisation; parliament sees least productive session in 15 years Save over 50% tax if new income tax slabs are implemented in Budget of 2017

Save over 50% tax if new income tax slabs are implemented in Budget of 2017