Deadline for filing Form 24Q extended: What if you still miss the deadline?

Notably, Form 16 and Form 24Q both have undergone updation last month.

The Central Board of Direct Taxes (CBDT) has once again extended the deadline for TDS statements. The due date for filing tax deducted at source (TDS) by employers, while Form 16 issue to employees and also the Form 24Q has been extended. Notably, Form 16 and Form 24Q both have undergone updation last month. While, even though the deadline for filing Form 24Q has been extended, but what happens if you still miss the scheduled date. Guess what! It's a long list of penalties, for missing this deadline. Let's find out!

CBDT last week mentioned that, with a view to redress genuine hardship of deductors in timely filing of TDS statement in Form 24Q on account of revision of its format and consequent updating of the File Validation Utility for its online filing, CBDT has ordered to extend the due date of filing of TDS statement in Form 24Q for financial year 2018-19 from 31st of May, 2019 to 30th of June, 2019.

That said, you only have 20 days left for this deadline of Form 24Q. If missed, you welcome a host of penalties.

What is Form 24Q?

When an employer pays salary to an employee, the Former is required to deduct TDS under section 192 of Income Tax Act. On quarterly basis, the employer needs to file salary TDS return in Form 24Q. There two parts in Form 24Q as well. The Annexure I involves deductee wise break up of TDS. This includes BSR Code of branch, Date on which challan deposited/Transfer voucher date, Challan Serial Number/DDO, Amount as per Challan, Total TDS to be allocated among deductees as in the vertical total of col. 326 and Total Interest to be allocated among deductees below.

While the Annexure II earlier included details Employee reference number (if available), PAN of the employee, Name of the employee, TDS Section Code, Date of payment/ credit, Amount paid or credited, TDS amount and Education Cess. This annexure has now been widened by CBDT.

What happens when you miss the deadline?

According to Income Tax department, a person who fails to file the TDS/TCS return or does not file the TDS/TCS return by the due dates prescribed in this regard has to pay late filing fees as provided under section 234E and apart from late filing fees he shall be liable to pay penalty under section 271H. In this part you can gain knowledge about the provisions of section 234E and section 271H.

Under section 234E, where a person fails to file the TDS/TCS return on or before the due date prescribed in this regard, then he shall be liable to pay, by way of fee, a sum of Rs. 200 for every day during which the failure continues. The amount of late fees shall not exceed the amount of TDS. TDS/TCS return cannot be filed without payment of late filing fees as discussed above. In other words, the late filing fees shall be deposited before filing the TDS return. It should be noted that Rs. 200 per day is not penalty but it is a late filing fee.

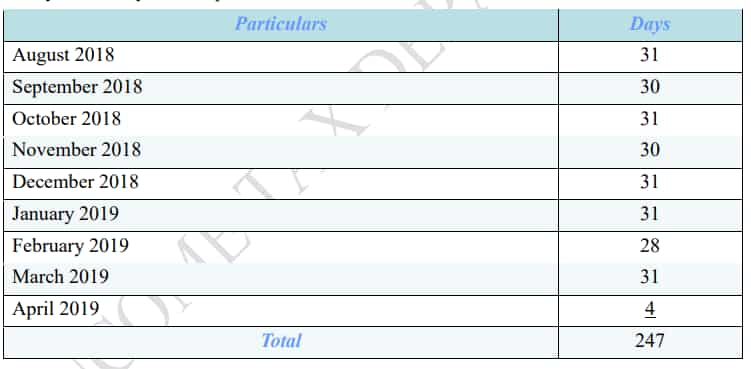

Here’s an example explained by the department.

Quarterly statement of TDS i.e. TDS return for the first quarter of the year 2018-19 is filed by Mr. Kapoor on 4-4-2019. Tax deducted at source during the quarter amounted to Rs. 8,40,000. What will be the amount of late filing fees to be paid by him for delay in filing the TDS return?

Due date for filing of TDS return for the first quarter of the year 2018-19 i.e. April 2018 to June 2018 is 31st July, 2018. The return is filed on 4th April, 2019, thus there is a delay of 247 days as computed below:

(Image source: IT Department)

The department highlights that, it can be observed that there is a delay of 247 days. Late filing fees under section 234E will be charged at Rs. 200 per day, thus for 247 days the late filing fees will come to Rs. 49,400.

Thereby, hurry up and file your TDS Form 24Q on time, or else face hefty penalties. Remember the more you delay, the more you bear!

03:46 PM IST

Selling shares, mutual funds? Here's how you must report your LTCG in ITR filing

Selling shares, mutual funds? Here's how you must report your LTCG in ITR filing  filing: Don't have login ID? This new PAN version can help you e-verify your ITR easily") Income Tax Return (ITR) filing: Don't have login ID? This new PAN version can help you e-verify your ITR easily

Income Tax Return (ITR) filing: Don't have login ID? This new PAN version can help you e-verify your ITR easily Have GSTIN, ITR? You can apply for loan up to Rs 1 crore, get approval in minutes

Have GSTIN, ITR? You can apply for loan up to Rs 1 crore, get approval in minutes  filing ALERT! Last date extended to August 31, 2019 in big relief for taxpayers!") Income Tax Return (ITR) filing ALERT! Last date extended to August 31, 2019 in big relief for taxpayers!

Income Tax Return (ITR) filing ALERT! Last date extended to August 31, 2019 in big relief for taxpayers!") Don't have your Form 16? Here's other alternative to file your Income Tax Return (ITR)

Don't have your Form 16? Here's other alternative to file your Income Tax Return (ITR)