ELSS vs NPS vs PPF - Retirement planning with Income Tax savings | Which one is a better investment?

PPF vs NPS vs ELSS arises among investors, who plan for their retirement-related investments and both options provide income tax exemption to an individual.

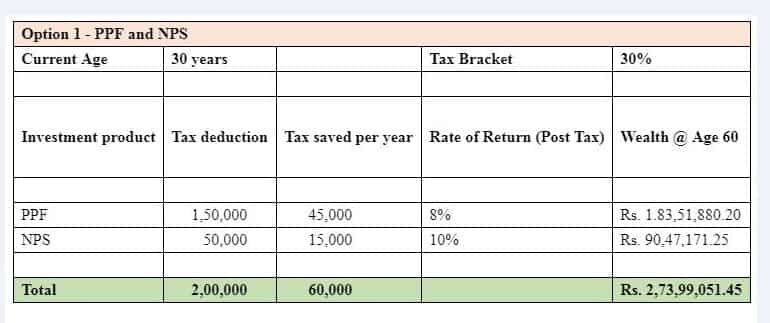

ELSS (Equity Linked Saving Schemes) and NPS are mainly known as a retirement-oriented savings vehicle options and ultimately serve the same purpose. But, the ground zero reality is different. Most of the investment experts say that for an investor who wants flexibility in investment Public Provident Fund (PPF) with ELSS offerings is a better option but for those who are investing only for their retirement, National Pension Scheme (NPS) is better as it yields around 10 per cent post-tax return. Ironically, investors opt for such products to save tax. Both the options are eligible for Tax deduction under section 80C of the Income Tax Act (ITA). Under section 80C, the maximum investment allowed in PPF is Rs 1.50 Lakh per annum. Additionally, an investor can invest in NPS under sec 80CCD (1B) up to a maximum of Rs 50,000 per annum. However, if we compare it with the normal PPF instead of PPF with ELSS offerings, we found later one is better as it maximises the return post-retirement or after 60 years of age.

Elaborating upon the benefit while opting the ELSS instead of PPF or NPS; Milin Shah, Head - Product Development & Planning at HappynessFactory said, "NPS is a product where one invests till 60 years of age with the option to invest till the age of 70 years. Post-retirement, the rule says that one can withdraw approximately 60 per cent of corpus as lumpsum without any tax impact and the remaining 40 per cent will be in the form of an Annuity and will be taxable, just like any other income." He said that the NPS allows an investor to diversify his or her portfolio between Equity, Government Securities and Fixed income instruments. "An investor can invest up to 75 per cent in Equity funds and this is a great advantage of NPS. While equity investments can be volatile, over the long horizons of a typical NPS investment, they are likely to generate higher returns than fixed income securities (Like PPF)," said Milin Shah of HappynessFactory.

Source: HappyFactory

Source: HappyFactory

Talking about the Ideal investment strategy in regard to PPF and NPS Milin Shah of HappynessFactory said, "Ideally, investors should choose an option depending upon their life situation and risk appetite. Someone, with a long investment time frame, can also look at investing in Equity Linked Saving Scheme offered by mutual funds (ELSS). ELSS are eligible for tax saving up to an investment of Rs.1.50 Lakh just like PPF."

Detailing the flexibility benefits in NPS against the PPF investment Kartik Jhaveri, Director — Wealth Management at Transcent Consultants said, "In PPF, an investor can't invest beyond Rs 1.5 lakh while in NPS an investor can invest any amount though he or she can claim tax benefit up to Rs 50,000 in one financial year." He said that in PPF, an investor has more flexibility as he or she can stop investment after 5 years and can withdraw the whole amount after 15 years while in NPS the whole amount is strictly fixed for a long period till the investor attains 60 years of age and the investor can't fish out the amount in between.

Source: HappyFactory

Source: HappyFactory

Speaking on the features of the ELSS, PPF and NPS Kartik Jhaveri of Transcent Consultants said, "PPF account matures after completion of 15 years. One may extend the term after 15 years by a block of another 5 years with or without making additional contributions. The maturity amount of PPF is 100 per cent tax-free. PPF is a 100 per cent Debt oriented product, guaranteed by the government, providing safety of capital. The current annual interest rate on PPF is 8 per cent."

08:23 PM IST

SBI PPF Account: Is premature withdrawal allowed in SBI Public Provident Fund? Here is what onlinesbi.com says

SBI PPF Account: Is premature withdrawal allowed in SBI Public Provident Fund? Here is what onlinesbi.com says PPF vs NPS: Why you should choose National Pension System ahead of Public Provident Fund

PPF vs NPS: Why you should choose National Pension System ahead of Public Provident Fund PPF and NSC account holders? This trick will help you fix your maturity amount, save income tax too

PPF and NSC account holders? This trick will help you fix your maturity amount, save income tax too PPF Alert: Top 5 basic details that every Public Provident Fund account holder must know

PPF Alert: Top 5 basic details that every Public Provident Fund account holder must know Money tips: Smart ways to save Income tax at the last moment; save over Rs 2 lakh

Money tips: Smart ways to save Income tax at the last moment; save over Rs 2 lakh