EPF interest rate hike ahead? You can become crorepati on basic pay of Rs 15,000

If an interest rate hike is on table ahead, then this will be beneficial to some 60 million employees - the EPFO manages retirement savings of up to Rs 11 trillion.

The wave of good news in 2019 has already begun and that too within just 2 days time! Notably, the first to see ache din will be salaried employees. It is believed that the retirement fund operator Employees Provident Fund Organisation (EPFO) is planning a new year gift for employees! Yes, interest rates of their provident fund scheme may well be hiked. With the news circulated it is expected to cheer up millions of employees. Currently, EPF allows an employee to enjoy 8.55% interest rate on their provident fund contribution from their monthly salary. Just like NPS, PPF, the government’s EPF scheme also aims in developing better future for salaried employees on their retirement. EPF is a corpus which is built by both employee and employers through regular monthly contribution. What is interesting to know for you as a subscriber is the gains you will make when you retire. Guess what! You can even become crorepati by the time your career gets over.

It was a buzz reported by Mint, with three officials raised hopes of a possible rate hike in EPF. Furthermore, at the very least, the interest rates will be retained at existing levels.

If an interest rate hike is on table ahead, then this will be beneficial to some 60 million employees - the EPFO manages retirement savings of up to Rs 11 trillion.

Let’s understand how much you gain from provident fund scheme on your retirement.

According to the EPF Act, an employee is eligible for benefits like provident fund, pension fund and insurance. A small fraction from an employee’s salary gets deducted in regards to provident under EPF, from the date of joining. However, an employee is not liable to give a portion of their salary under EPF, if their organisation has a workforce below 20 employees.

In case of an employer, they have to contribute a percentage in employee’s pension fund along with provident fund which an employee can avail upon retirement.

Features of EPF!

Among many benefits, one of the key opportunity under EPF is that interest earned on them are fully tax exempted. Also, withdrawals on maturity or after completion of 5 years service are fully tax free for an employee under EPF.

Going ahead, an employee also enjoys tax deduction of Rs 1.5 lakh under section 80C of Income Tax Act.

In fact, EPF also allows premature withdrawal on emergency cases like medical treatment and financial issues.

It is needs to be noted that, an employee can only withdraw their EPF amount after 2 months of their resignation from an organisation.

In case of demise, the nominee receives EPF wealth 2 months after the employee is declared legally dead.

An employee can also withdraw EPF balance, if they are no longer in position to work.

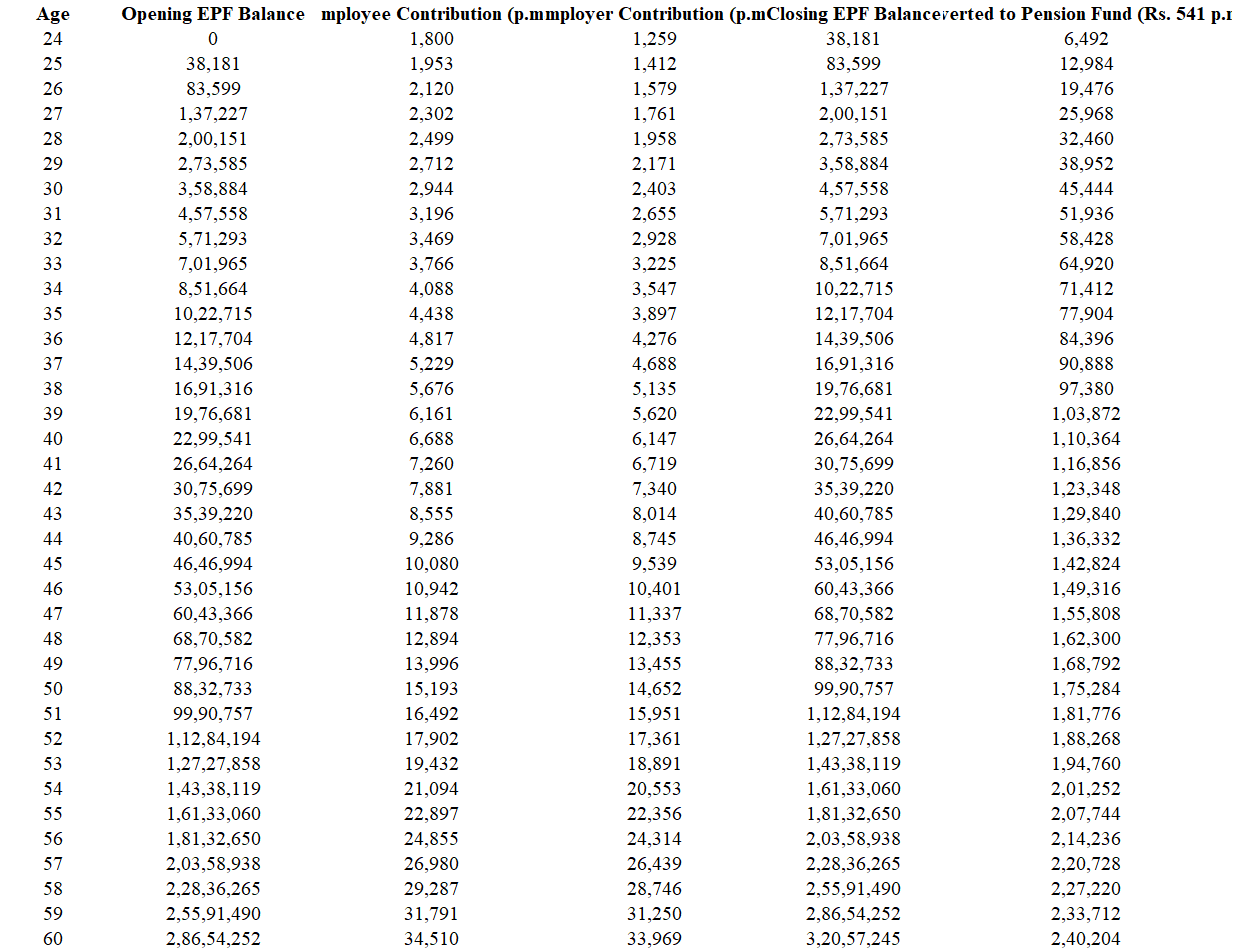

Now that everything is said and done, let’s calculate how much do you actually contribute under EPF, and how much you will receive on your retirement on this scheme.

Both employee and employer have to pay 12% fixed rate on basic pay plus dearness allowance. For example, if an employee’s basic pay is Rs 15,000 then he or she will see Rs 1,800,160 (12% of Rs 15,000) deduction on their monthly pay.

Similarly, an employer will also contribute Rs 1,800 in employee’s funds. This amount would be then split into two portions - firstly 8.33% to EPF which would come around Rs 1,249.5 and remaining 3.67% under EPS resulting in Rs 541.

Apart from this, there is also EPF administration costs of 0.65%, EDLI (Employee Deposit linked insurance) of 0.5% and EDLI administration costs of 0.01%.

Firstly, one should note that employees who earn less than Rs 15,000 per month will fall under the bracket of EPF contribution. In 2014, the threshold limit under EPF was changed from Rs 6,500 to Rs 15,000. If you are earning above Rs 15,000 then you are not eligible for any pension funds. However there are many reports circulated since 2016, that government may be looking to increase this limit up to Rs 21,000, however, no clarity has been given till now.

Hence, on Rs 15,000 basic salary your monthly contribution comes around Rs 1800 under EPF.

Thereby, let’s assume you are at the age of 24 and invest Rs 1,800 in your EPF account and decided to retire at the age of 60. Also, Rs 1800 contributed by employer, will lead your EPF wealth to jump over whopping Rs 3.20 crore. Meanwhile about Rs 2.40 lakh will be your pension fund at the age of 60.

While the above calculation is based on current interest rate under EPF, interestingly, if government does hike the rates for this tool then definitely good days have arrived for employees who look for retirement savings.

If you want to check your EPF balance, here’s how you can do it.

For checking an EPF balance, an employee must ensure that their employer has activated their Universal Account Number (UAN) which is allotted by EPFO.

Step 1 - Once you are have your active UAN pin, then login to EPFO portal www.epfindia.gov.in

Step 2 - Scroll down to the homepage and below you will find a 'Service' section under which 'Member Passbook' option available.

Step 3 - After clicking on Member Passbook, a login page will appear before you. Enter the UAN number you have along with a password.

One can even access their EPF balance via SMS and missed calls at EPFO. For SMS - an employee must send message as EPFOHO UAN ENG on mobile number 7738299899. In case of missed calls - one can call on toll free number 011-22901406 from their registered number in EPF account.

There is also m-sewa app of EPFO which will help in reviewing your EPF account balance.

11:04 AM IST

EPFO alert! New Year gift from Modi government - Good news is here!

EPFO alert! New Year gift from Modi government - Good news is here! EPFO employees alert! Know your Diwali PLB bonus, here's how to calculate it

EPFO employees alert! Know your Diwali PLB bonus, here's how to calculate it How you can transfer your EPF account; check steps and why you need to do it

How you can transfer your EPF account; check steps and why you need to do it Have EPF account? Here’s why you must also get UAN ID - Find out what EPFO says

Have EPF account? Here’s why you must also get UAN ID - Find out what EPFO says  Don't have cash for marriage, education or buying a house? Shed your worry, withdraw funds from EPF account; here is how

Don't have cash for marriage, education or buying a house? Shed your worry, withdraw funds from EPF account; here is how