Existing borrowers not happy with loan rates; will EMIs come down? Controversy decoded

Crux of the matter: Why banks are not passing on the benefits of rate cuts to borrowers.

The disappointment over lending rates charged by banks has put the spotlight on the Reserve Bank of India (RBI) as the central bank is now being questioned by Supreme Court to break 10-months' silence on why the lenders were not passing on the benefits of the rate cuts to citizens. The apex court's reaction comes after a complaint was filed that banks did not reduce their floating interest rates on existing loans during the time of rate cuts. The anger of citizens is valid, considering that when rate cuts and status quo decisions were announced, these had created possibilities for a reduction in benchmark MCLR which would lead to downward trend in lending rates. This would in turn make EMIs of borrowers fall. But now tables have turned, situation is changed and India is on the edge for a possible policy rate hike - an eventuality raised by RBI itself - on the back of soaring crude oil prices and depreciating rupee. Finally, the complaint has reached the highest levels and now all eyes are watching what RBI's next move will be.

A Times of India report says that a petitioner, MoneyLife Foundation, told the court that it wrote to RBI last October complaining, “whenever the interest rate goes down, new borrowers are offered a lower interest rate with respect to similar small loans in the fields of housing, education and consumer goods against principles of natural justice and equity. However, there is minimal or often no reduction in interest rates of old borrowers."

From the contents of the letter, it is clear that banks were charging one set of borrowers a different rate of interest and another one from the earlier ones.

Reportedly, the loss to consumers aka borrowers is well in excess of Rs 10,000 crore for denial of every 1% of the benefit (reduction in floating interest rates).

It would be wrong to say that RBI did not take the petitioners letter into consideration. The report mentions that RBI replied on December 26 last year that the issues raised were under consideration of the banking regulator. However, the petitioner stated that till date the decision remains a secret.

Notably, RBI was already familiar with the matter of lenders way of deciding interest rates on small loans like home, personal and vehicle.

Way before the petition was filed, RBI in August 2017, policy showed massive disappointment in banks MCLR benchmark methods.

RBI said on August 02, 2017, “The experience with the Marginal Cost of Funds Based Lending Rate (MCLR) system introduced in April 2016 for improving the monetary transmission has not been entirely satisfactory, even though it has been an advance over the Base Rate system.”

Ex-RBI governor Raghuram Rajan in June 07, 2016 raised a similar issue. He said, “The banks seem to be suggesting they are not going to attract a whole lot of new credit if they reduce rate, so why not stay with the existing borrowers and so on. That was why we moved from the base rate to MCLR because that would mean a more automatic reduction in rates when deposit rates came down.”

Thereby, RBI even put in place an Internal Study Group to review the working of MCLR.

Therefore, on February 08, the group recommended that, there is a need to move to one of the three external benchmarks, viz., the treasury bill rate, the certificate of deposit (CD) rate and the RBI’s policy repo rate, which is outside the control of an individual bank, from April 1, 2018. The decision on the spread over the external benchmark should be left entirely to the commercial judgment of banks, with the spread remaining fixed all through the term of the loan, unless there is a contractually pre-defined credit event.

Feedback from banks on those recommendation showed challenges for RBI.

The lenders boldly mentioned that, retail customers would resist a shorter (quarterly) reset, particularly in a rising interest rate cycle, because of the increase in equated monthly instalments (EMIs) or longer repayment period with uniform EMIs.

However, one should take into account that banks were rebellious in passing over the benefits of lower policy repo rate to customers in the form of interest rates on their loans.

RBI introduced the new lending rate MCLR regime in April 2016 with an aim to ensure that the banks pass on the benefits of RBI's rate cut to their customer in faster pace.

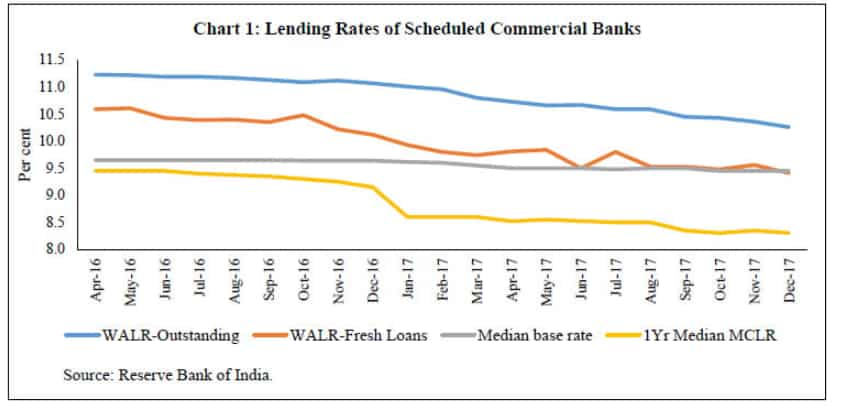

Data compiled by RBI in regards to Weighted Average Lending rate (WALR) of scheduled Commercial banks (SCB), reveals that the quantum of reduction in lending rate was less by banks when RBI followed a policy repo rate cut.

RBI under Rajan’s reign, kept repo rate unchanged from April 2016 till September 2016 at 6.50%. During that time, WALR shifted from 11.26% to 11.17%. Also these were the times when banks credit growth were on downward trend due to heavy stressed assets, higher provisions and weak earnings of banking systems.

Then the first cut was made in October 2016, by the RBI newly appointed governor Urjit Patel by a 25 basis points. Since then till June 2017, the policy repo rate stood at 6.25%. In these period, the WALR only came down by 45 basis points from 11.15% in October 2016 to 10.70% by end of June 2017.

In July 2017 made another cut of 25 bps taking policy repo rate to 6%. However, WALR came down by 40 basis points.

Further, the RBI’s group revealed that from January 2015 to December 2017, the policy repo rate has come down by 2 percentage points, while WALR on outstanding loans below 1.58 percentage points and WALR on fresh rupee loans by 2.04 percentage points.

Meanwhile, from April 2016 to December 2017, the repo rate was down by 0.75 percentage point, while MCLR for 1 year term was below 1.15 percentage. However, WALR for outstanding rupee loans were down by 0.94 percentage points and WALR for fresh rupee loans were just below 1.06 percentage points.

Following which, it was noted that, while some discretion remained with banks, the MCLR has continued to suffer from the same flaw in that transmission to the existing borrowers has remained muted as banks adjust, in many cases in an arbitrary manner, the MCLR and/or spread over MCLR, which has kept overall lending rates high in spite of the monetary policy being accommodative since January 2015.

Coming to current scenario, now that banks credit growth has finally started to pick up from its six decade low of 3.5% as on March 2017.

Last available data from RBI reported that a print of 13.5% yoy growth was seen in banks credit as compared to a low of 3.5% yoy last witnessed in March 2017.

A recent report by CIBIL provides keen insights into the current state of consumer loans.

The report highlighted that: (1) Retail loans (including NBFCs) grew 27% yoy led by 26% growth in live accounts touching 100 mn accounts. The flattish average ticket size is attributed to a change in the loan mix towards credit cards, personal loans and consumer durable loans.

However, from June 2018, everything has become different, while banks credit growth accelerates, the policy repo rate also have risen.

A Kotak Institutional Equities report said, “ Rising interest rates, tight liquidity, negligible difference in origination costs between MCLR/market rates has resulted in this shift. This would have further increased considering the recent events that have unfolded in the money market post the IL&FS default.”

So one should really ask the question themselves, that is there any possibility for cut in lending rates hence lower EMIs.

The October 2018 policy, where RBI maintained a status quo hints for possibility in reduction of EMIs on home loans, personal loans and vehicle loans.

Adhil Shetty, Co-founder and CEO, BankBazaar.com laid out what the impact of an actual rate hike would have been on borrowers! Lesson? RBI choice of status quo is the best thing to happen to them short of an interest rate cut.”

A status quo in the policy rates means that deposit rates would stabilise or marginally increase. This increase will contribute to driving up the interest rates on bank fixed deposits as well.

Shetty said, "We have recently seen interest rates of small savings schemes for the current quarter go up by 30-40bps."

When deposit rates are high in banks, their saving schemes become a lot more attractive hence motivating customers to invest their savings with them. If funds in the form of deposits continue to come in, then banks would not have to entirely depend on borrowing from RBI, they can actually utilize the deposits to sanction loans.

Loans are bread and butter of every banks, hence, heavy deposits help them in getting funds so that it can be used for retail loans which is currently at booming stage.

To lure customers in taking small size loans, this encourages banks to trim down their lending rates, hence, your EMIs. However, this comes as a good news to new borrowers, but there seriously needs an strict action to banks way of levying lending rates to old borrowers.

Each lending and deposit rate decided by any bank has a direct relationship with policy repo rate.

When banks borrow funds from the central bank during shortages, they are currently paying a higher interest rate, which is 6.50%. This was not the case 2 policy meets ago as they just paid 6%, which was till June, 2018. So, now with a 50 basis points hike borrowing from RBI becomes costly for banks.

Lending interest rates

Just like every other commodity, money has also its own way of price. That price for money is known as interest rate.

The one who saves, for them interest rate is a return on their investment, which a bank pays on the money the customer has deposited.

These interest rate on deposits, is a price paid by banks and other financial institution to customers for using their money to lend to individuals or businesses.

Vice-versa, for a person who borrows money from banks, the interest rate is an extra amount that needs to be paid for borrowing. Simply put, the borrower repays the loan known as principal plus some extra money (interest) to banks for using their funds. Now these interest rates received from borrowers is an earning for lenders.

Decisions by depositors and borrowers for either savings or borrowings - affect consumption and investment decisions, and ultimately aggregate demand and overall economic activity.

08:40 PM IST

EMI calculation: Should you pay or not? Anil Singhvi explains what home loan, auto loan, other borrowers should do

EMI calculation: Should you pay or not? Anil Singhvi explains what home loan, auto loan, other borrowers should do EMI Moratorium Latest News: What it is? What it means for car, home and other loans? Should you postpone payment or keep paying? Check best advice for you

EMI Moratorium Latest News: What it is? What it means for car, home and other loans? Should you postpone payment or keep paying? Check best advice for you Took home loan, car loan from this bank? Good news for you - Check details

Took home loan, car loan from this bank? Good news for you - Check details SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers

SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers RBI steps will ease pressure on the financial system: Amitabh Chaudhry, Axis Bank

RBI steps will ease pressure on the financial system: Amitabh Chaudhry, Axis Bank