Here's how to convert Rs 1600 saving on your home loan EMI into Rs 17 lakh!

State Bank of India, reduced its MCLR rates by 0.90% points across all tenure loans

State Bank of India (SBI) on Sunday slashed its marginal cost of funds based lending rates (MCLR) by 90 bps giving a chance to home buyers to get home loans at cheaper rates.

State Bank of India, reduced its MCLR rates by 0.90% points across all tenure loans bringing down the effective home loan rates to 8.60% from 9.10% per annum.

Thus, with the cheaper home loans, you will save a significant amount per month on EMIs.

How to use that saved money? What if the you get back more than half of the loan amount back just by saving and investment?

Here's how?

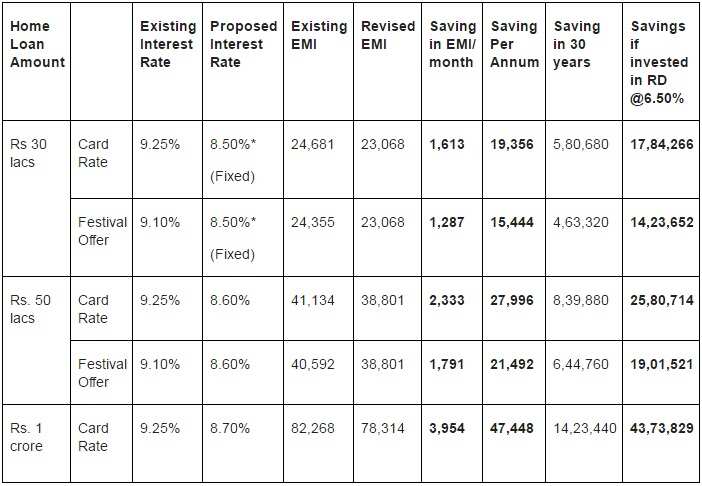

On Tuesday, SBI said for instance, you have taken a loan of Rs 30 lakh for a tenure of 30 years. According to their calculations, your revised EMI will be Rs 23,068 with the fixed interest rate at 8.55% (1 year MCLR+50 bps) as compared to old interest rates which were at 9.25%. Earlier the EMI amount was Rs 24,681.

Currently, the bank is offering fixed interest option (8.5%) for loan up to Rs 30 lakhs only. Though, floating interest rate option is also available for the said amount starting from 8.6%.

This shows, in one month you are saving Rs 1,613 taking a total of Rs 19,356 in one year. And in 30 years, you are saving Rs 5,80,680. Suppose, if you invest the saving in Recurring Deposit at 6.50% interest, you are saving Rs 17,84,266, which is more than half of your actual loan amount i.e. Rs 30 lakh.

The above was the case as per card rate. Now, during festival offer, for the same Rs 30 lakh loan, the bank was giving interest at 9.10%, which means your monthly EMI was 24,355. But, with the revised rates at 8.5%, your monthly EMI is 23,068. Which means, still you are saving Rs 1,287 per month, Rs 15,444 in one year and Rs 4,63,320 in 30 years. If you invest the savings in RD at 6.50%, you are getting Rs 14,23,652 back.

Now, supposedly, for the loan of Rs 50 lakh, the existing interest rate as per card rate is 9.25% for the time period of 30 years. This means your monthly EMI is Rs 41,134. With the revised rates at 8.6%, the monthly EMI comes at Rs 38,801. Thus, it shows that monthly EMI saving is Rs 2,333, yearly saving is Rs 27,996 and savings in 30 years is Rs 8,39,880.

If you invest the savings in RD at 6.5%, you are getting Rs 25,80,714 back, which is again more than half of the original loan amount of Rs 50 lakh.

Presently, the bank was offering 9.10% interest rate as festive offer. Calculating the savings for the same Rs 50 lakh loan amount, the EMI amount was Rs 40,592. With the new rates i.e. 8.6%, the monthly EMI comes to Rs 38,801. The saving amount per month is Rs 1,791, yearly is Rs 21,492 and Rs 6,44,760 in 30 years. Investing the savings in RD at 6.50%, you are getting Rs 19,01,521 back in your account.

In the last situation, if the loan amount is Rs 1 crore and the interest rate is 9.25%, your current EMI for the month is Rs 82,268. But, with the revised interest rate which is 8.70%, your monthly EMI comes to Rs 78,314. Now your monthly saving on EMIs will be Rs 3,954, yearly Rs 47,448 and Rs 14,23,440 in 30 years. Investing the savings in RD at 6.50% will be Rs 43,73,829.

Source: State Bank of India

Keep investing your savings in other financial instruments and get huge returns.

01:36 PM IST

SBI Life COVID-19 death claim: Useful coronavirus tips to make SBI Life Insurance claim

SBI Life COVID-19 death claim: Useful coronavirus tips to make SBI Life Insurance claim  interest rate cut by up to 50 bps; check sbi.co.in for latest details") OnlineSBI: SBI fixed deposit (FD) interest rate cut by up to 50 bps; check sbi.co.in for latest details

OnlineSBI: SBI fixed deposit (FD) interest rate cut by up to 50 bps; check sbi.co.in for latest details SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers

SBI interest rates on loans slashed by whopping 75 bps, passes on entire RBI repo rate cut to borrowers Withdraw cash without your SBI debit card, ICICI Bank debit card

Withdraw cash without your SBI debit card, ICICI Bank debit card SBI business opportunity for you: Earn this much money every month, plus big allowance

SBI business opportunity for you: Earn this much money every month, plus big allowance