Income Tax: Here's how you can save Rs 46,000 more tax on your income

But one should know that the only investments made in the period April 1, 2016 to March 31, 2017 can be claimed as deduction from the total income.

It is "that time" of the year when every taxpayer is looking for tax saving options that optimises tax burden at the same time maximises the returns.

But one should know that the only investments made in the period April 1, 2016 to March 31, 2017 can be claimed as deduction from the total income. After this date it will not give you the tax benefit in FY 2016-17.

So before the financial year ends, here's how you can save under various investments:

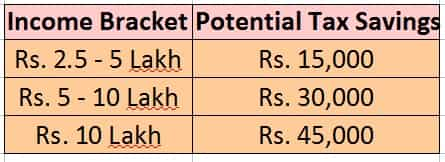

Speaking with Zeebiz, Archit Gupta, Founder & CEO of ClearTax.com, explained that under section 80c, if your income is Rs 9 lakh, the investments can reduce your income maximum up to Rs 1.5 lakhs and if you are in 30% tax bracket it can save up to Rs 46,350 (Rs 45000+ Rs 1,350 cess).

(a) Equity Linked Saving Scheme (ELSS) – ELSS are diversified mutual funds with lock in period of year years. They give you double benefit in the form of tax saving investment and are also exempt from long term capital gain tax. ELSS being equity oriented have the potential to earn higher returns.

(b) Deposit in PPF Account – PPF is also a long term saving scheme by the government with the lock in period of 15 years. Anyone can open PPF in SBI, Post office or other Banks. The interest income from PPF and proceeds from maturity of PPF both are exempt from tax.

(c) Tax Saving Fixed Deposit – It is like any other fixed deposit in the bank or post office but it has the lock in period of five years. The interest earned is taxable.

(d) Sukanya Samriddhi Account- This is a government saving scheme for the girl child. The investment is locked till your girl child turns 18.The amount received on Maturity amount is Tax free.

(e) Senior Citizen Saving Scheme- It is a saving scheme by the government for senior citizens. This Scheme gives regular income to senior citizens. The maturity period is five years. The interest earned is taxable.

(f) Claim Tuition Fees – Tuition fees paid to any school, college, university or educational institute situated in India for the education of children is allowed as deduction from the income but for maximum up to two children.

(g) Life Insurance Premium – The annual Premium paid for life insurance for self, spouse or children is also deductible from income. The entire premium amount paid during the financial year irrespective of the period to which it relates. For instance, if you have paid single LIC premium of Rs 25,000 on 20th Feb 2017 for the period of one year up to February 19, 2018. You can claim the whole amount in your return for FY 2016-17 as the payment is made before 31st March, 2017, though the period relates to next financial year.

(h) Repayment of Home Loan Principal – The repayment of the principal of a loan taken to buy or construct a residential property is also eligible for the deduction.

(i) Contribution to PF – The contribution to PF by the employer is tax exempt while the employee’s contribution is deductible from the income.

02:22 PM IST

Income Tax Alert! Filing ITR online? Ensure e-verification before logging out; step by step guide

Income Tax Alert! Filing ITR online? Ensure e-verification before logging out; step by step guide Alert! Three Month Tax Saving Exercise: PPF, loans, insurance to education, top investment options for taxpayers

Alert! Three Month Tax Saving Exercise: PPF, loans, insurance to education, top investment options for taxpayers  Planning to opt for new income tax slabs 2020? You can still claim this NPS account benefit

Planning to opt for new income tax slabs 2020? You can still claim this NPS account benefit Changes required in Income Tax law to benefit homebuyers; check what experts think

Changes required in Income Tax law to benefit homebuyers; check what experts think Yet again, Finance Minister pays heed to Zee Business Managing Editor Anil Singhvi's call, extends ITR filing deadline

Yet again, Finance Minister pays heed to Zee Business Managing Editor Anil Singhvi's call, extends ITR filing deadline