US is the new favourite destination for India Inc

Commerce and Industry Minister Nirmala Sitharaman said Prime Minister Narendra Modi has directed that every proposal that entails some expenditure must lead to job creation and need to include jobs estimate.

Key Highlights:

- 100 Indian firms have employed across 50 states of the US

- India Inc invested about $18 billion in US

- India Inc's job creation grows at a paltry 2.25% in the country

Rate of growth of job creation by India Inc's continues to be a cause of concern in the country. They seem to have found a new favourite spot for employment and considering the recent data the United States is the most preferred place.

According to a report titled 'Indian Roots, American Soil', released by Confederation of Indian Industry (CII) on November 14, Indian firms have created over 113,000 jobs in the US and also invested $18 billion in the country.

100 Indian firms have employed across 50 states of the US with New Jersey being the top spot having 8,572 jobs generated, followed by Texas with 7,271 jobs, California with 6,749 jobs, New York with 5,135 jobs and Georgia with 4,554 jobs.

Indian Ambassador to the US, Navtej Sarna, on the latest numbers said that the Indian firms play an important part in the US' economy and make valuable contributions to it.

"The presence and reach of Indian companies continue to grow each year as they invest billions of dollars and create jobs across the United States," he added. As many as 87% of these companies are interested in hiring more employees locally in the next five years in US.

It was noted that two Indian firms, Tata Group and Infosys, stole the limelight in the US. Earlier in May, the Bengaluru-based IT giant Infosys stated that it intended to hire 10,000 employees in the US and also set up four technology hubs in the country.

While corporates enhance their presence in the US market, the rate of generating new employment in India is growing at a slower pace year after year.

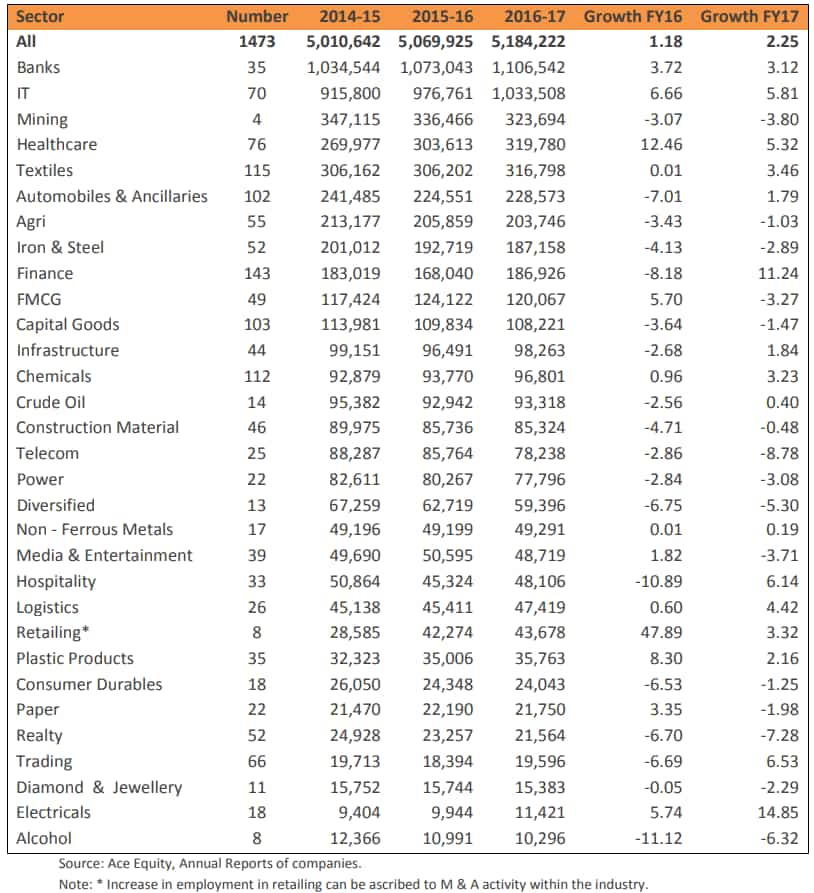

Data compiled by Care Ratings for 1,473 companies highlighted that aggregate employment stood at 51,84,222 in FY17 – growing at a paltry 2.25% compared to 50,69,925 in the previous fiscal.

Five sectors namely banks, IT, mining, healthcare and textiles collectively accounted for nearly 60% of this total employment.

Banks (including both private and state-owned) hired 11,06,542 employees in FY17 versus 10,73,043 employees in FY16 and 10,34,544 employees in FY15.

However, the growth rate was lower in FY17 at 3.12% compared to the rate of 3.72% in FY16. Similar was the case of IT and healthcare that hired 10,33,508 and 3,19,780 employees in FY17 compared to 9,76,761 and 3,03,613 employment in FY16 respectively.

Growth rate in these two sectors stood at 5.81% and 5.32% in FY17 versus 6.66% and 12.46% in FY16. Not only this, IT firms has seen decline in hiring during the first half of fiscal year 2017-18 (FY18) also.

Tata Consultancy Services (TCS), Infosys, Wipro, HCL Technologies, Tech Mahindra and Cognizant Technologies together employed 1,243,777 people at the end of the September quarter. In the first quarter these firms together employed 1,247,777 people, this translates to a net reduction of 4,157 employees.

The National Association of Software and Service Companies (Nasscom) highlighted reason for a slowdown in the growth of hiring in Indian IT firms is the change in business model as these companies have started working on newer technologies such as cloud computing, which needs fewer employees. Many of them have adopted automated tools that perform mundane tasks that were earlier performed by an army of engineers.

Also a US-based research firm HFS stated that about 7 lakh low skilled workers in IT and BPO industry in India are likely to lose their jobs to automation and artificial intelligence by 2022.

In Care Ratings view, this becomes a major cause of concern for a developing country like India and calls for some proactive measures. It said: "The recent initiative by the government to push infrastructure in the country is likely to pave way for creation of jobs that might change the scenario going forward. Further, as shown in the study, growth cannot foster employment generation and has to be backed by strong investment and new business opportunities."

Earlier, even Singapore's Deputy Prime Minister Tharman Shanmugaratnam has guided Indian government to undertake labour reforms on an urgent basis to create employment opportunities.

Shanmugaratnam at the Delhi Economics Conclave said, "India's biggest challenge is jobs. It is a real challenge going forward because India has lost a lot of time, it has lost a lot of time because you have legislation, employment legislation which is anti-employment."

05:53 PM IST

India Inc hails Trump's visit; hopes to raise India-US economic engagement

India Inc hails Trump's visit; hopes to raise India-US economic engagement What India Inc expects from US President Donald Trump's maiden visit

What India Inc expects from US President Donald Trump's maiden visit Ahead of Budget 2020, PM Narendra Modi meets top executives of India Inc.

Ahead of Budget 2020, PM Narendra Modi meets top executives of India Inc. Corporate tax reliefs to spur growth, create jobs: India Inc

Corporate tax reliefs to spur growth, create jobs: India Inc India Inc mourns Arun Jaitley's demise; Here's what they said

India Inc mourns Arun Jaitley's demise; Here's what they said