Income tax returns (ITR) filing: How to save tax; amazing tips to make your money stay in your wallet

Income tax returns (ITR) filing: As the investments made are generally with a long term perspective, it is important that informed decisions are made based on the tax benefits available as well as risk appetite, time horizon and liquidity requirements of the investors.

filing: How to save tax; amazing tips to make your money stay in your wallet")

With the end of financial year just around the corner, many of the tax payers would be scurrying to make sure that the tax deductible investment avenues have been completely utilized, so that tax efficiency is achieved. As the investments made are generally with a long term perspective, it is important that informed decisions are made based on the tax benefits available as well as risk appetite, time horizon and liquidity requirements of the investors. Here is a quick look on the tax savings options available under the Income-tax Act:

1.0) Deduction under section 80C (Maximum limit upto Rs.1.5 Lakhs p.a.)

Section 80C provides a wide range of tax savings investment opportunities. Within the basket of Section 80C the investments can be divided into two categories viz; investments with fixed and assured returns which include PPF, NSC, Senior Citizens Savings Scheme, endowment life insurance plans, etc. and investments linked to market which are primarily the equity-asset class. This includes ELSS and ULIP, pension plans and NPS.

| Tax- Savings Investments | Remarks |

|---|---|

| Life Insurance Policies: Premium paid on the life insurance policies issued by LIC or any other registered Insurance company is allowed as deduction. | Life insurance premium in respect of policy on life of tax payer, spouse and any child of taxpayer is allowed. However, insurance premium should not exceed prescribed percentage (generally 10%) of sum assured. This is a long term investment with limited surrender value but provides for financial security. |

| Public Provident Fund (PPF): PPF is the most popular savings avenue for several investors as it gives higher returns (holds a combined limit for minor & self) and safe avenue. | It is an EEE scheme (Exempt-Exempt-Exempt). The investment in fund is tax deductible, Interest accrued is tax exempt and withdrawal from the account is tax exempt. Please note Budget 2018 proposes repeal of Public Provident Fund Act 1968 (PPF Act) and its coverage under the Government Savings Banks Act 1873. As such it is expected that the Exempt-Exempt-Exempt scheme shall also be continued under the new proposed Act even for FY 2018-19 and onwards. However, the present protection for non-attachment of the contributions made to PPF shall not be available for the new contributions under the Government Savings Bank Act. |

| ELSS: Equity-Linked Savings Scheme is diversified equity mutual funds with differentiating features. | The same is subject to lock in period of 3 years. However, it may be noted that decision on investment in ELSS should be based on certain fundamentals like the performance of the scheme, its ratings, etc.Dividends are tax exempt.It is pertinent to note that Budget 2018 has proposed to introduce tax at the rate of 10% from FY 2018-19 on long term capital gains exceeding Rs. 100,000, earned on sale of listed equity oriented mutual funds. |

| Sukanya Samriddhi Account: This offers the highest tax-free return with a sovereign guarantee. This account can be opened by parents or legal guardians of a girl child (below the age of 10 years) in any post office or nationalized banks listed with RBI for this scheme. | Any payment from the scheme shall not be liable to tax. It is an EEE scheme (Exempt-Exempt-Exempt). The investment is tax deductible, Interest accrued is tax exempt and payment from the account is tax exempt. |

| Repayment of Housing loan, stamp duty, registration fees | The principal repayment is eligible for deduction subject to cumulative limit. Further, amount paid towards stamp duty, registration charges for purchase of house is also eligible for deduction |

| National Savings Scheme | These have a lock in period of 5 years & can be purchased from post offices. Interest earned is taxable. However, interest re-invested (for all years except last year) is eligible for deduction u/s 80C |

| Deposit in Senior Citizen Savings Scheme 2004 | Eligible for higher interest than the normal bank deposits. |

| Term Deposit with scheduled bank/post office. | Interest is taxable with a minimum tenure of 5 years but highly liquid. |

| Assessee's own contribution to recognized provident fund and superannuation fund | Interest earned is tax-free but has long term tenure. |

| Tuition Fees | Payment of admission fees or college fees to university, college, educational institution in India for full time education of any two children. |

2.0) Deduction under section 80CCD

One of the lesser known deduction includes contribution made by the employer under section 80CCD(2) to the notified pension scheme which is not covered within the overall cap of Rs. 150,000 for cumulative deductions under section 80C, 80CCC & 80CCD(1).

Under Section 80CCD(2), an employee can get deduction in respect of employer's contribution towards his NPS account up to limit of 10% of his salary. This deduction is in addition to the deduction provided under section 80CCD(1), wherein deduction is provided to the taxpayer for his own contribution to NPS, within the overall limit of Rs. 150,000.

From financial year 2015-16 and onwards, in case the NPS contribution by the taxpayer, he can still avail of the additional deduction of Rs. 50,000 under the newly inserted provision of section 80CCD(1B). Therefore, the total tax benefits that can be claimed for NPS under Section 80CCD (1) and Section 80CCD (1B) equals to Rs. 2 Lakhs for the financial year 2017-18.

3.0) Deductions in respect of donations to certain funds, charitable institutions, etc. (Section 80G):

The donations made to approved funds and charitable institutions are eligible under section 80G up to 10% of the adjusted total income. The eligible deductions are generally eligible for deduction of 50%. It is a general practice amongst the employers that they do not consider deduction while computing tax on the salary income and issue of Form 16 and the employees need to claim the same in the tax return. Further, the taxpayer should note that no deduction under this section is allowable in case of amount of donation if exceeds Rs 2,000/- unless the amount is paid by any mode other than cash.

4.0) Deduction in respect of contributions to political parties

One of the interesting deduction, which many people are not aware is that contributions made to registered political parties are also eligible for deduction under the Income Tax Act (section 80GGC).

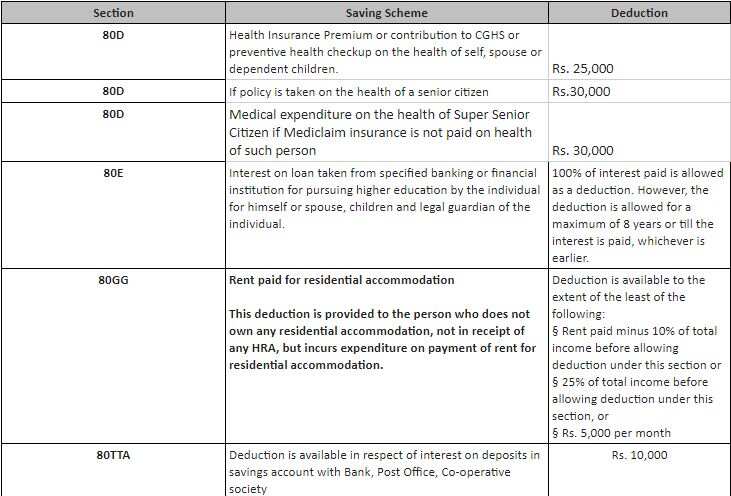

5.0) Other Deductions

6.0) Deduction of interest incurred on housing loan

Interest paid on housing loan is eligible for deduction under section 24(b) of the Income-tax Act. While there is no limit of interest deduction for let out / deemed let out property, the deduction is restricted to Rs. 2,00,000 in case of self-occupied property. This loss would be eligible for set-off against your salary income and other income during the year. However, from financial year 2017-18 the maximum house property loss, which can be set off against the other heads of Income in the same financial year is Rs. 200,000. The balance loss under the head Income from House Property from house property shall be carried forward for set off in the subsequent 8 assessment years under the same head of income.

The income tax act provides ample of deductions and tax saving schemes. It is advisable to take maximum advantage of the tax breaks available and optimise your tax outflow.

(Suresh Surana, Founder, RSM Astute Consulting Group)

04:18 PM IST

Income Tax: 3 deadlines you shouldn't miss this month

Income Tax: 3 deadlines you shouldn't miss this month Income Tax Payer? Save your money! Top 10 tips for ITR filers to profit from

Income Tax Payer? Save your money! Top 10 tips for ITR filers to profit from Income Tax alert! Last date to do this work is October 31, check all details here

Income Tax alert! Last date to do this work is October 31, check all details here ITR filing: Crorepati taxpayers grew 20% in Assessment Year 2018-19: Tax data

ITR filing: Crorepati taxpayers grew 20% in Assessment Year 2018-19: Tax data Are you a taxpayer? Beware! This Income tax refund fraud will lead to big money loss

Are you a taxpayer? Beware! This Income tax refund fraud will lead to big money loss